ESSAY

Arvind SmartSpaces Ltd

4 May 2026

1. Why This Company Is Worth Your Attention Right Now

On March 9, 2026, Pirojsha Adi Godrej, Executive Chairman of Godrej Properties, personally spent Rs 40.7 crore buying shares of Arvind SmartSpaces through a BSE bulk deal. He had zero prior stake in this company. The seller was HDFC Capital Affordable Real Estate Fund-1, an institutional fund exiting its position. This was not a Godrej Properties transaction. It was Pirojsha’s personal money going into a real estate developer that his own group does not run.

That is an unusual signal worth paying attention to. A person who runs one of India’s biggest real estate businesses, who sees hundreds of deals and projects every year, who understands the sector’s cycle better than most, chose to put personal capital into a smaller developer at a time when the broader real estate sector had corrected significantly. This report is an attempt to understand what he likely saw.

The investment case for Arvind SmartSpaces is not about the Pirojsha signal alone. It is about a genuinely good business, run by a credible promoter family, with a clean balance sheet, a proven execution track record, and a multi-year growth runway that the market is currently undervaluing because of the way real estate revenue recognition works. The Pirojsha purchase is the hook. The fundamentals are the reason to stay.

2. Business Understanding

Who Is Arvind SmartSpaces

Arvind SmartSpaces is the real estate development arm of the Lalbhai Group, a $2 billion Ahmedabad-based conglomerate with roots going back to 1897. The group has historically run businesses across textiles, chemicals, and engineering. The real estate business was spun off in 2008 as a separate entity and listed in 2015.

The company is primarily known for two things. First, it is the dominant branded real estate developer in Ahmedabad, a market with limited organised competition and strong brand loyalty. Second, it has a track record of 100% on-time project delivery, which in a sector notorious for delays, is a genuine differentiator that commands customer premium.

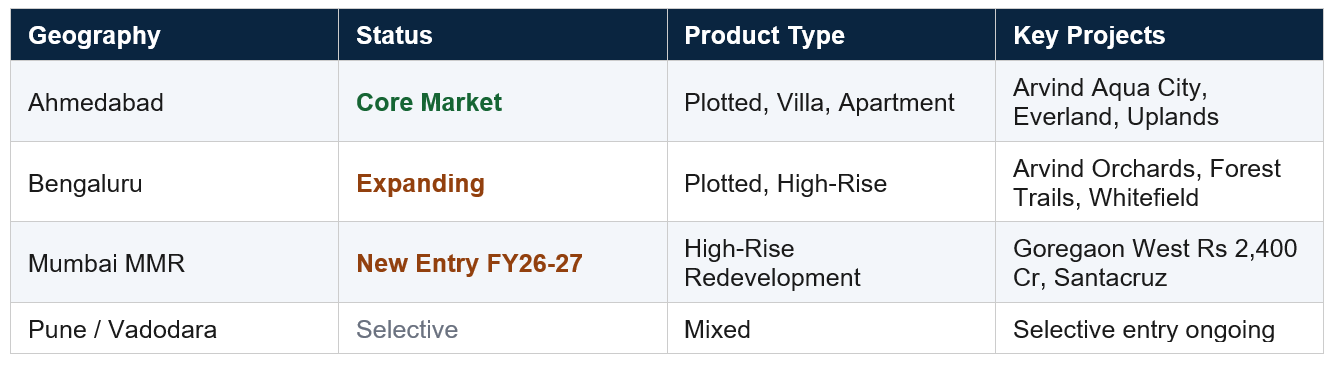

What They Build and Where

The product portfolio has two broad categories. Horizontal development includes plotted land, villa townships, and low-rise villa communities. This has historically been Arvind’s strength, particularly in Ahmedabad where branded plotted developments sell out within hours of launch. Vertical development includes mid-segment apartment complexes and high-rise residential towers. The company is deliberately shifting its mix toward 60 to 70 percent vertical over the next 4 to 5 years as it expands into Mumbai and Bengaluru.

The Asset-Light Business Model

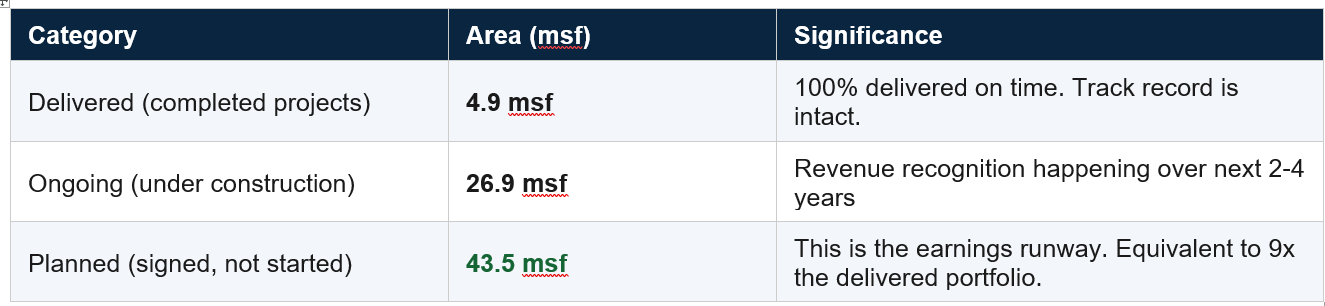

This is one of the most important things to understand about Arvind SmartSpaces. Unlike developers who aggressively acquire land on their own balance sheet, Arvind primarily uses Joint Development agreements and Joint Venture structures where landowners contribute the land and Arvind contributes the brand, execution capability, and capital. Under JD agreements, Arvind does not need to pay for land upfront. This dramatically reduces balance sheet risk and keeps debt low. It is the primary reason the company can show net debt of only Rs 79 crore despite running 26.9 million square feet of ongoing projects.

The asset-light model does have a trade-off. Margins are lower than outright land purchase, and Arvind must share revenue with the landowner. Management has recently been adding more outright acquisitions to the mix to balance this, particularly in Bengaluru where three of their four new projects added in 9M FY26 were acquired outright.

The Pipeline

The planned pipeline of 43.5 msf is the most important number on this page. It represents the future earnings of the business that are not yet visible in reported financials. This is the number Pirojsha was almost certainly looking at.

3. The Critical Thing to Understand About Real Estate Accounting

Before you look at any financial number in this report, you need to understand one thing. Reported revenue in a real estate company is not the same as sales. When Arvind SmartSpaces sells you a flat in their Everland project, they do not book that revenue immediately. Under Indian accounting standards, they recognise revenue only when the project reaches certain completion milestones, typically possession or specific construction stage percentages. The booking can happen in FY26, but the revenue might appear in FY28 or FY29.

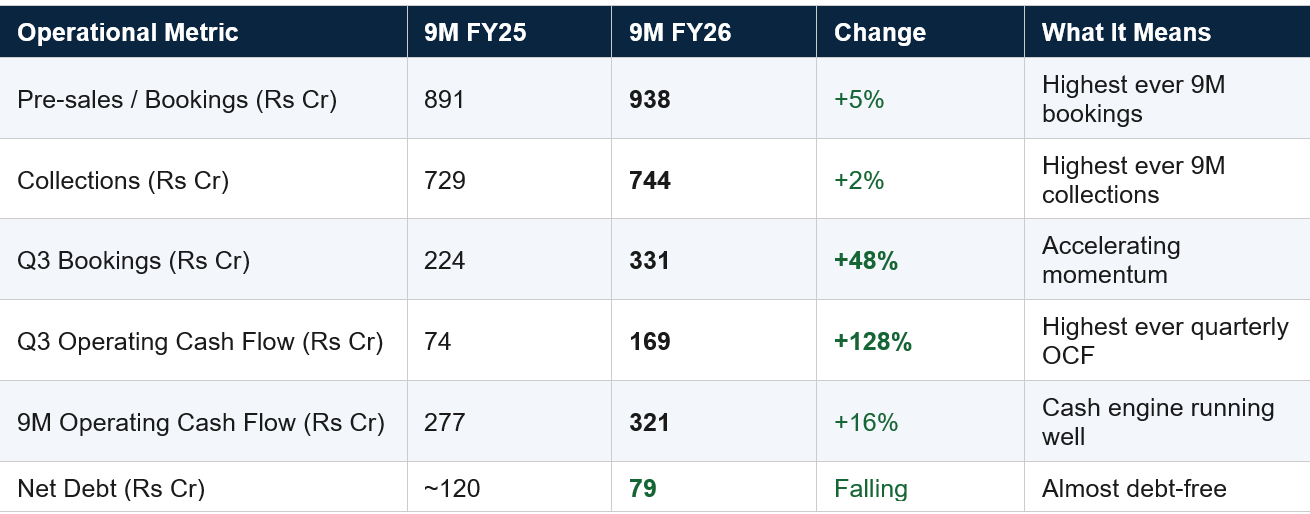

This creates a systematic disconnect between operational performance, measured by bookings and collections, and reported financial performance, measured by revenue and profit. In periods when a company is launching and selling aggressively, reported financials look weak while the business is actually doing very well. The cash has been collected. The earnings just have not been reported yet.

This is the single most important insight for understanding Arvind SmartSpaces. The stock fell 37% from its 52-week high largely because Q2 and Q3 FY26 reported revenue declined YoY. But bookings were at all-time highs and operating cash flows were growing at 128% YoY. The market sold the reported revenue. The smart money bought the bookings.

Arvind SmartSpaces estimates unrealised operating cash flow from its current project pipeline at over Rs 4,581 crore, expected to materialise over the next 4 to 5 years. This is revenue that has already been contracted but not yet reported. The stock is currently priced as if this pipeline does not exist.

4. Financials

Operational Metrics (The Real Story)

Reported Financials

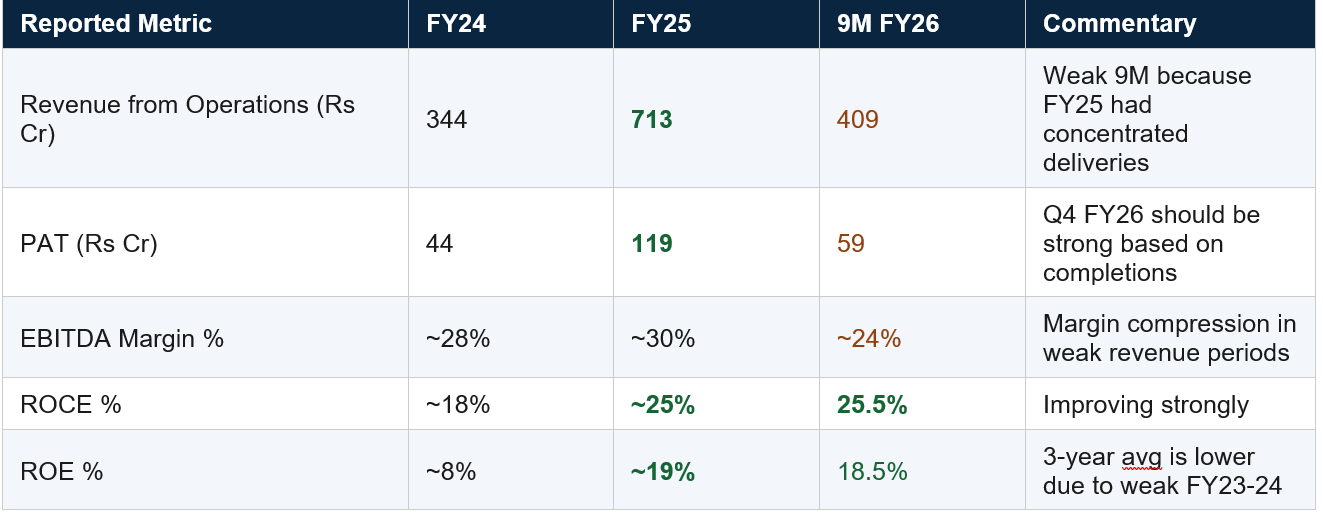

The reason 9M FY26 reported revenue is Rs 409 crore versus Rs 550 crore in 9M FY25 is not because the business is performing worse. It is because FY25 had concentrated project completions, particularly in the first half, generating strong recognition. FY26 has had strong bookings but the completions and therefore the revenue recognition falls more heavily in Q4 and into FY27. This is a timing mismatch, not a business deterioration.

5. Management and Promoters

The Lalbhai Family

Arvind SmartSpaces is run by the Kasturbhai Lalbhai Group, one of India’s most respected industrial families. The group has operated continuously since 1897 across textiles, chemicals, engineering, and now real estate. Kulin Lalbhai, son of Sanjay Lalbhai, serves as Non-Executive Chairman of Arvind SmartSpaces. The promoter family holds 53.8% of the company as of the latest shareholding data, which has increased from 49.82% in September 2025. Promoters increased their stake by 4.01% in the most recent quarter.

The group has a reputation for ethical governance, clean financials, and conservative capital allocation. Zero promoter pledging is reported. No related party transactions of concern. The parent Arvind Limited paid a minor penalty of Rs 8.14 lakh to exchanges for a delayed independent director appointment in Q2 FY26, which is an administrative compliance matter and not a governance red flag.

New CEO Transition

In February 2026, Kamal Singal, who led the company for over 15 years, stepped down as Managing Director and was succeeded by Priyansh Kapoor. Singal remains on the board as Director of Strategy and Investments. This transition was described as a structured succession process initiated in July 2025. Early management commentary from Kapoor has maintained the same strategic priorities with a continued focus on asset-light growth and geographic expansion.

Any CEO transition carries execution risk, particularly during a period of geographic expansion. This is the most important management risk to track over the next four to six quarters.

Capital allocation grade: A-. The decision to pursue an asset-light JD-heavy model rather than aggressive land banking has been validated by the clean balance sheet. Promoter stake increase of 4% in a single quarter is a strong confidence signal. The new CEO transition is the only question mark.

6. The Growth Thesis

Catalyst 1: Mumbai Entry

For most of its history, Arvind SmartSpaces was a Gujarat-and-Bengaluru story. Mumbai, India’s most valuable real estate market, was absent from the portfolio. That changed in FY26. As of April 2026, the company has three projects in the Mumbai Metropolitan Region, including the Goregaon West high-rise signed on April 7, 2026, with a revenue potential of Rs 2,400 crore. This is the company’s largest single project ever. Mumbai projects typically carry higher absolute revenue and margins than Ahmedabad, given land costs and selling prices. A successful execution in Mumbai would materially re-rate the business.

Catalyst 2: The Revenue Unlock from the Pipeline

The company has unrealised operating cash flow of over Rs 4,581 crore from its current project pipeline. This revenue will flow into reported financials over the next 4 to 5 years. As each project crosses completion milestones, the reported numbers will start reflecting what the bookings data has already shown for the past two years. FY27 and FY28 are expected to be the years when this catch-up becomes visible to the broader market.

Catalyst 3: Business Development Momentum

Management has guided Rs 3,500 to Rs 4,000 crore of new business development additions in FY26. As of 9M FY26, they had already achieved Rs 2,510 crore, or 62.5% of annual guidance, with January 2026 alone seeing Rs 860 crore of additions in Bengaluru. Each new project added today is a future earnings stream that is not visible in the current stock price. The January BD alone in a single month exceeded what many peers add in a full quarter.

Catalyst 4: India Residential Real Estate Cycle

India’s residential real estate market is in a multi-year upcycle driven by rising urban incomes, aspirational demand, and the structural shift from renting to ownership. The plotted development and villa township segment, where Arvind is the dominant brand in Ahmedabad, has seen particularly strong demand from buyers seeking lifestyle upgrades in the post-pandemic period. This is a demand driver that is independent of any single company’s execution and benefits Arvind disproportionately given its brand position.

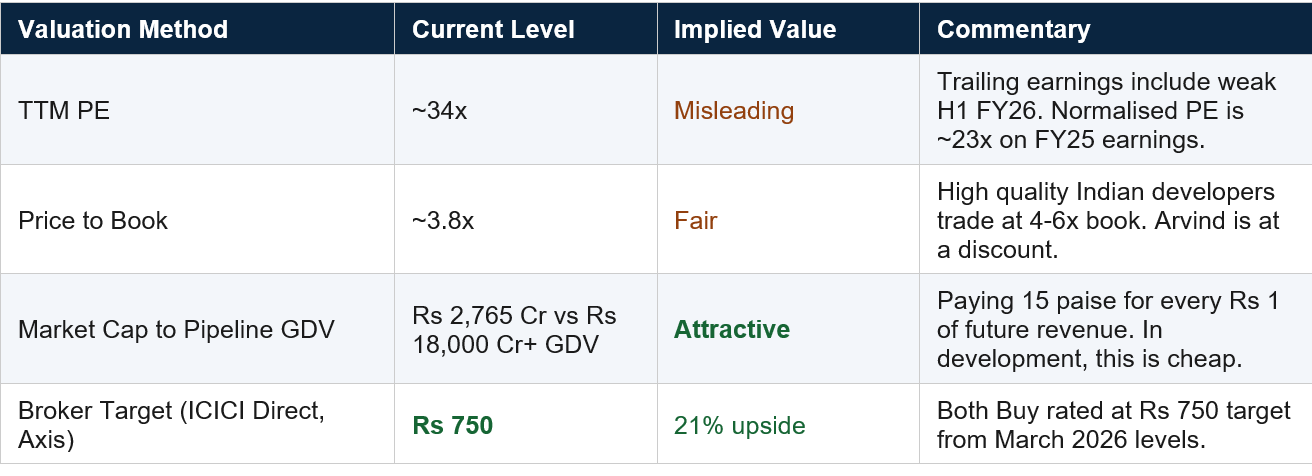

7. Valuation

How to Think About Valuing a Real Estate Company

Traditional PE ratios are misleading for real estate developers because reported earnings are a lagged and lumpy reflection of the business. The three correct frameworks are pre-sales based NAV, price to book, and a normalised earnings yield based on a forward estimate of what earnings will look like once the current pipeline delivers.

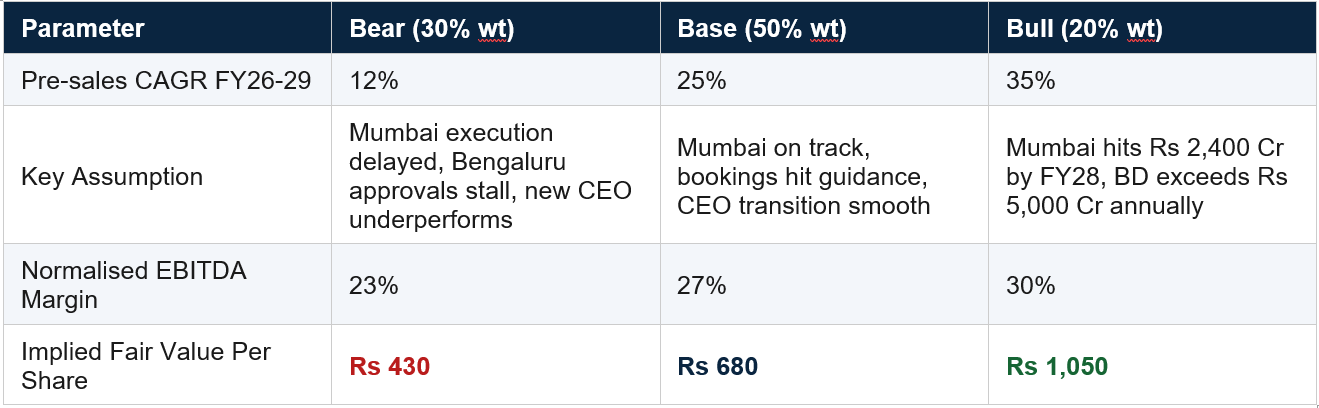

Scenario Analysis

Probability-weighted fair value: 30% x 430 + 50% x 680 + 20% x 1,050 = Rs 129 + Rs 340 + Rs 210 = Rs 679 per share.

At the current CMP of approximately Rs 620, the stock is trading at a modest 9% discount to the probability-weighted fair value of Rs 679. The compelling entry zone is Rs 520 to Rs 560, which would represent a 17 to 23% discount to fair value, which is the minimum margin of safety appropriate for a real estate developer with execution dependencies in new geographies.

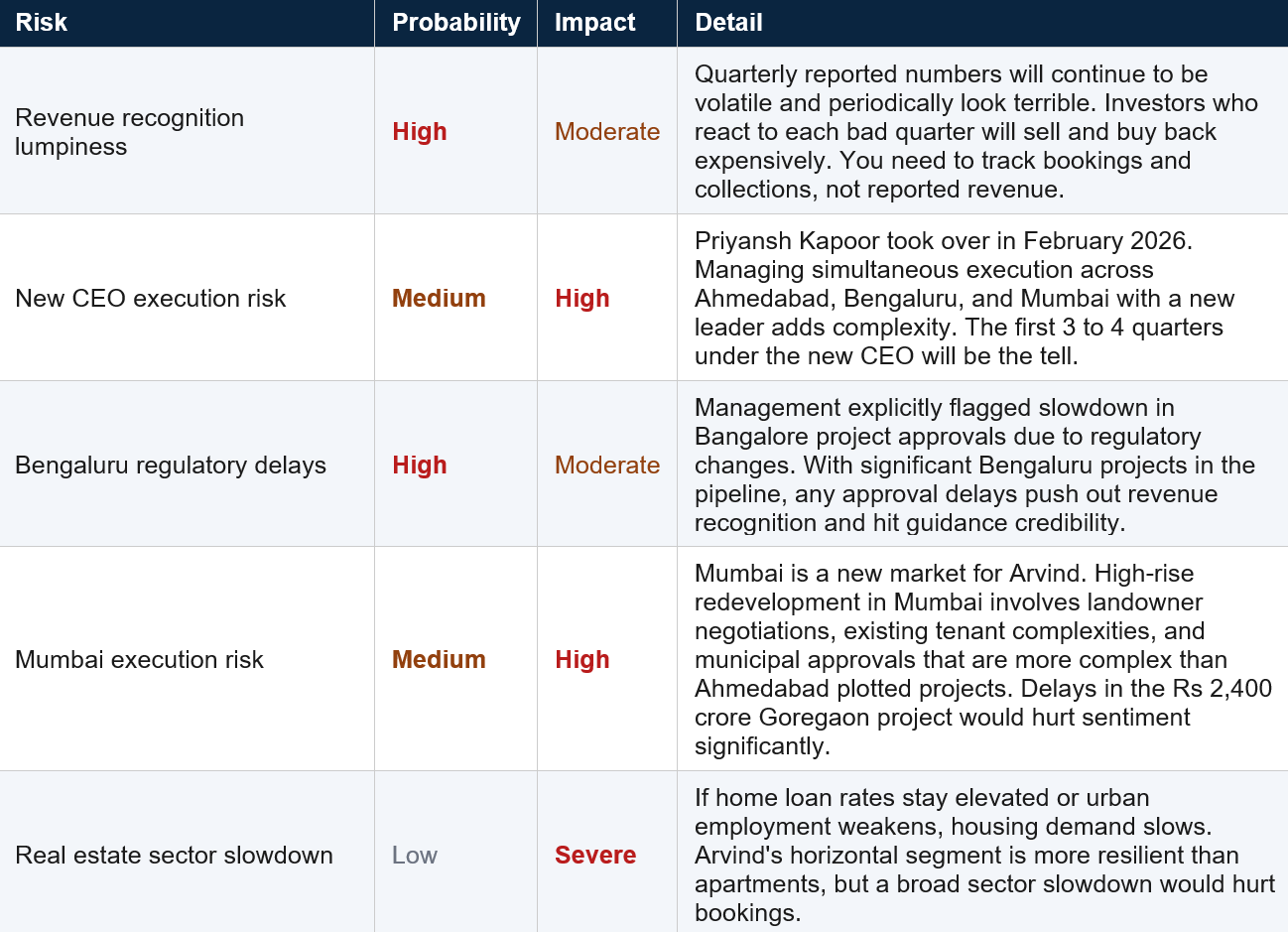

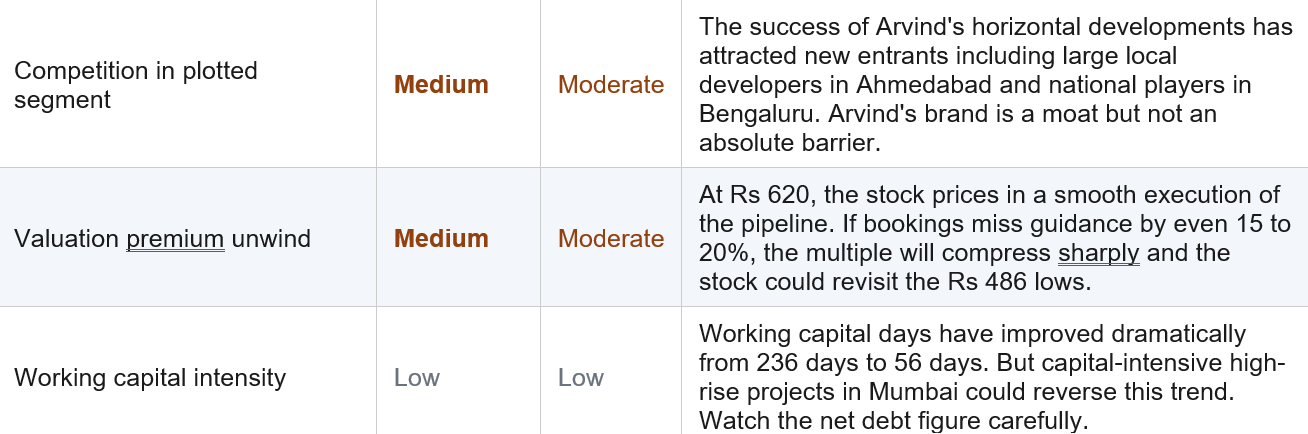

8. Risks

DISCLAIMER

This research report has been prepared by Compound with Raunak for educational and informational purposes only. It does not constitute investment advice, a solicitation, or an offer to buy or sell any security. The author is not a SEBI registered investment advisor. All financial data, estimates, and projections contained in this report are sourced from publicly available information including BSE and NSE filings, company investor presentations, analyst reports from Axis Securities, ICICI Direct, and MarketsMojo, company concall transcripts, and financial media. While reasonable care has been taken to ensure accuracy, no guarantee is made regarding the completeness or accuracy of the information provided. Past performance of any security does not guarantee future results. Investing in equity markets involves significant risk, including the possible loss of your entire principal. Readers should conduct their own due diligence and consult a SEBI registered financial advisor before making any investment decisions. The author may or may not hold positions in the securities discussed. This report was prepared in May 2026 and reflects information available as of that date.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.