ESSAY

Ashish Kacholia Has Been Buying This Defence SME for Three Consecutive Quarters. Here is the Full Breakdown.

16 April 2026

Before we get into the company, let us talk about the signal.

Ashish Kacholia manages a publicly disclosed portfolio of over Rs 2,400 crore. He is not a momentum trader. He does not chase narratives. His track record in small and mid cap stocks over two decades speaks for itself.

When an investor of that calibre buys a stock three consecutive quarters in a row, the third purchase happening through quiet open market accumulation after the stock had already corrected 42% from its peak, that is worth paying attention to.

Here is the complete buying trail for Techera Engineering India Limited:

He entered near the all-time high. He kept buying all the way through a 42% correction. His blended average cost across all three tranches is approximately Rs 195 to Rs 215.

That is what conviction looks like in practice.

Now let us look at what he is actually buying.

What Techera Engineering Actually Does

Techera Engineering India Limited is a Pune-based precision engineering company incorporated in October 2018. They design and manufacture the tooling and jigs used to physically build aircraft.

Not the aircraft themselves. The infrastructure required to manufacture the aircraft.

When HAL assembles a Tejas fighter jet, they need precision jigs and fixtures to hold the fuselage components in exact alignment during assembly. They need layup tools to shape the carbon fibre composite wing panels. They need ground support equipment to maintain the aircraft once it is in service. Techera makes those things.

Their product portfolio includes assembly toolings, jigs, fixtures, maintenance and repair toolings, ground support equipment, and precision machined components. They also provide automation system solutions.

The company holds AS9100D:2018 certification alongside ISO 9001:2015. AS9100D is the aerospace quality management standard used globally. Boeing, Airbus, HAL, and every serious defence PSU requires it from their suppliers. You cannot get into this supply chain without it. Techera spent seven years building that certification and the customer relationships that come with it.

Three manufacturing plants. Over 90,000 sq ft of combined space. A newly commissioned 6.2 metre, 5-axis KEN high-precision machine — one of the largest of its type in India. A dedicated TechEra Design Centre for aerospace customers.

They are not just a job shop. They own the design process. That distinction matters enormously for margin sustainability.

The Market They Are Sitting In

India’s defence budget has grown at above 10% annually for the last five years. The government has put in place hard domestic procurement mandates under the Defence Acquisition Procedure. Atmanirbhar Bharat is not just a slogan in defence — it is backed by policy, budget, and blacklists for foreign suppliers where Indian alternatives exist.

The Tejas programme is the centrepiece of this.

The Cabinet Committee on Security, chaired by Prime Minister Modi, cleared an order for 97 additional Tejas Mk1A jets worth Rs 62,000 crore on August 19, 2025. HAL confirmed this in an official NSE exchange filing the same day. This is in addition to the original 83-jet Mk1A order placed in 2021 for Rs 48,000 crore. Total Tejas orders now stand at 180 jets across both tranches.

Every single one of those jets requires tooling to manufacture. HAL cannot ramp production from 8 aircraft per year to the targeted 16 to 24 per year without the tier-2 and tier-3 precision tooling supply chain scaling alongside it.

Digital penetration of private sector suppliers in India’s defence manufacturing is still extremely low. Most tooling has historically been done in-house by PSUs. That is changing. HAL is actively developing private sector suppliers. Techera is one of them.

The Three Catalysts Worth Watching

Catalyst 1: Direct IAF Procurement

In the investor call transcript filed on NSE on December 19, 2025, Managing Director Nimesh Desai described a meeting he had at Vayu Sena Bhawan with a senior Air Vice Marshal. He said the Indian Air Force is moving to direct central procurement from Techera, bypassing the existing multi-tier intermediary chain.

His exact words from the transcript: “The central purchasing it means everything they will be required in India wherever they want they will be procuring from there only. So that’s a great news... now the connection is going to be direct.”

This is not a signed contract. It is a pipeline discussion. But the significance is real. Moving from tier-3 supplier to direct IAF vendor collapses the margin dilution from intermediaries. It also creates a direct long-term customer relationship with India’s largest single buyer of aerospace tooling.

Catalyst 2: Private Jet Tooling MOU

In the same December call, Desai confirmed Techera is in discussions to sign an MOU with India’s first private jet manufacturer to supply the complete tooling set for an entire aircraft programme. He described it as “a training aircraft initially and then it will get converted into a business aircraft.”

This is a different kind of contract than a per-component PSU order. Full aircraft tooling programmes last years, require ongoing support while the manufacturer keeps building, and create an annuity-style revenue stream for the tooling supplier.

Catalyst 3: Fresh Order Win, April 8, 2026

On April 8, 2026, Techera received a domestic order for aerospace composite layup tools worth Rs 4.87 crore to be executed by September 30, 2026. This was announced via BSE filing.

At Rs 56 crore TTM revenue, a single Rs 4.87 crore order represents approximately 8.7% of a half year’s revenue. This is not noise. Defence tooling orders of this type also tend to be repeat business because the same composite layup tool requires refurbishment and replacement over the aircraft’s operational life.

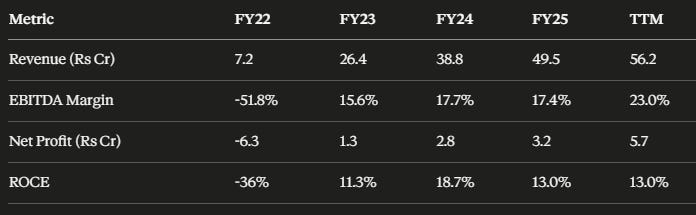

The Financial Picture

Revenue has compounded at 90% over three years. Let us look at the actual numbers.

The revenue growth is real and the profitability trajectory is improving. TTM net profit of Rs 5.7 crore is the highest in the company’s history. EBITDA margins have expanded to 23% on the TTM basis, up from 17.4% in FY25.

One important pattern to understand before you react to the quarterly numbers: This business is highly seasonal. Every single year, H2 (October to March) is significantly stronger than H1 (April to September) because government defence orders are typically executed and billed toward year-end.

If you see a weak September quarter result and panic, you are misreading the business. Every H1 for this company has looked weak. Every H2 has delivered. The Mar 2026 full year results, when they are announced, will tell you the real story of FY26 performance.

Management guided 30 to 40% revenue growth for FY26, with EBITDA margins targeted at 22 to 23% in H2 and long-term margins expected to reach 22 to 25%.

Cash flow is improving. FY25 operating cash flow was Rs 4.46 crore versus net profit of Rs 3.17 crore, a conversion ratio above 100%. This is the first year the cash flow picture has looked clean. Prior years had negative OCF.

The Forensic Checks

What is clean:

Promoter pledging: Zero. Not a single share pledged.

Auditor: No change, no qualified opinion.

Restatements: None in any available period.

Debtor days: Improved significantly from 178 days (FY23) to 104 days (FY25). The receivables quality is getting better, not worse.

What needs monitoring:

Promoter selling in December 2025. Promoter holding dropped from 42.25% to 39.62% in the December quarter. In the investor call, MD Nimesh Desai confirmed he personally sold shares to repay personal debts. His exact words: “I need to clear my personal debts and that is the reason I have diluted but there is no way our focus is 100% in the organizations.”

He was transparent about it. The explanation is personal, not operational. But promoters selling for personal reasons on any listed company is a yellow flag that needs to stay on the radar.

DII collapse. This is the single most unexplained data point in this analysis. DII holding went from 12.51% in March 2025 to 0.02% by December 2025. Institutions essentially walked out entirely in three quarters. At the same time Kacholia was walking in. What did institutions see that prompted that level of exit? I do not have a satisfying answer to this. It is an open question that deserves resolution before building a large position.

The Valuation Reality

Let me be direct about this. The stock is expensive.

At a current price of approximately Rs 190, the PE is around 88x trailing earnings. Price to Book is approximately 6x. EV/EBITDA is above 30x.

For a company doing Rs 56 crore in TTM revenue, these are demanding multiples. The market is pricing in significant growth materialising over the next two to three years. If the IAF direct procurement discussions convert to orders, if the private jet MOU closes, if FY26 full-year results show the margin expansion management guided, the current valuation starts to look more reasonable. If those catalysts do not show up in the numbers, there is meaningful downside.

Scenario analysis on FY27 earnings:

Bear case (25% weight): Revenue Rs 80 crore, margin 18%, EPS approximately Rs 8.7, target PE 20x = Rs 174. Down from current price.

Base case (50% weight): Revenue Rs 95 crore, margin 22%, EPS approximately Rs 12.5, target PE 28x = Rs 350. Up approximately 85%.

Bull case (25% weight): Revenue Rs 115 crore, margin 25%, EPS approximately Rs 17, target PE 35x = Rs 595. If IAF direct supply and private jet MOU both close.

Probability-weighted fair value: approximately Rs 330.

At Rs 190, the stock is trading at a 42% discount to the base-case fair value. But that fair value is entirely dependent on order conversion. This is not a value stock. It is a growth and execution story trading at a growth multiple.

The Risks. Read These Before Forming Any View.

1. Valuation leaves no margin for error. At 88x PE, if growth disappoints by even one quarter, the stock can re-rate sharply. There is no cheap valuation cushion here.

2. NSE SME listing. Daily trading volumes are regularly below 50,000 shares. Entering and exiting at any meaningful size is genuinely difficult. Bid-ask spreads can widen significantly during corrections.

3. Promoter sold shares for personal debt. This was confirmed explicitly by the MD in a public call. The explanation is plausible. The optics are still poor for a company this early in its listed life.

4. DII exit is unexplained. Institutional holding went from 12.51% to 0.02% in three quarters. Retail is absorbing what institutions are selling. This demands explanation.

5. Revenue is lumpy and project-dependent. There are no long-term supply contracts disclosed. Revenue depends on order flow from defence PSUs which can be delayed by government approval timelines, budget releases, and programme changes outside Techera’s control.

6. Company is six years old. The entire financial track record has been generated during a period of strong tailwinds for defence spending and Make in India. This company has never been tested in an austerity cycle or a defence budget cut.

7. Pipeline is still pipeline. The IAF direct procurement, the private jet MOU, and the L&T-adjacent order were all described as discussions in December 2025. None of these have been announced as signed contracts. Until they convert, they are in the thesis but not in the numbers.

8. ROCE dropped from 18.7% to 13% despite revenue growth. The FY25 capex push (Rs 38 crore in fixed assets) has not yet generated the return on capital it needs to justify. The new machinery needs to show up in revenue and margins before ROCE recovers. Watch FY26 and FY27 ROCE closely.

This article is published by CompoundWithRaunak purely for educational and informational purposes. It does not constitute investment advice, a buy or sell recommendation, or a solicitation of any investment decision.

I am not registered with SEBI as an Investment Adviser, Research Analyst, or in any other regulated capacity. Nothing in this article should be construed as professional financial or investment advice.

All data used in this article is sourced from publicly available information including NSE and BSE filings, company investor call transcripts filed with the exchange, and financial data platforms including Screener.in. While best efforts have been made to ensure accuracy, no warranty is made regarding completeness.

Investing in equity markets involves risk of capital loss. NSE SME-listed stocks carry significantly higher risk than mainboard stocks, including substantially lower liquidity and limited public information. Past financial performance of any company does not guarantee future results.

I may or may not hold a position in the securities mentioned in this article. Please conduct your own independent research or consult a SEBI-registered investment advisor before making any investment decision.

Follow on Instagram for more research.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.