ESSAY

CMS Info Systems

26 May 2026

Snapshot

Why I picked this one apart

Most people have never heard of CMS Info Systems, yet almost all of us have used it. Every time an ATM actually has cash in it, there is a good chance CMS loaded that machine. It is the largest cash management company in India, and for years it was a quiet compounder that nobody discussed.

What pulled me back to it was a contradiction. In the space of a few months, this small company won mandates from SBI, ICICI Bank and HDFC Bank, the three largest banks in the country. Over the same period, the stock fell about 35 percent. A business winning the biggest names in Indian banking while its own price gets cut by a third is exactly the kind of contradiction worth a few hours of work. What follows is that work, laid out in full.

1. The business, in plain terms

CMS makes money in three ways, and the whole story is about the mix shifting from the first toward the third.

Cash logistics

This is the legacy engine. Armoured vans, cash in transit, ATM replenishment, retail cash pickup. CMS is the clear market leader here, holding roughly a 42 percent share of India’s organised cash logistics market. It is steady, it throws off cash, and the margins are thin. For FY26 this segment did about 1,597 crore of revenue.

Managed services

Here CMS does not merely move cash, it runs the entire ATM operation for a bank on an outsourced basis: forecasting cash needs per machine, managing uptime, handling compliance. The bank offloads the operational headache and pays a fee. CMS has climbed from the number five player to number three in this space, and the segment did about 1,036 crore in FY26.

Technology and payment solutions

This is the future, and the reason the story is interesting. CMS has built an AI driven monitoring platform called HAWKAI that watches thousands of ATM and bank sites in real time. By the company’s own disclosures it has prevented over 2,700 incidents and stopped more than 900 burglaries in a single year, and HAWKAI revenue has roughly doubled to about 200 crore in two years. Technology and payment solutions now make up about 16 percent of services revenue, up from 12 percent a year earlier. The company is deliberately turning from a fleet of cash vans into a technology platform.

The entire investment debate sits in one sentence: can a cash logistics company become a technology company faster than physical cash fades.

2. Industry and the cash question

The obvious fear is that India is going cashless. UPI is everywhere, digital payments are exploding, and the lazy conclusion is that anyone touching physical cash is doomed. The data is more nuanced. Cash in circulation and the number of ATMs are both still growing in absolute terms, even as cash loses share of total transactions. Outsourced ATMs in India stood at roughly 120,000 in late 2025 and are expected to climb toward 170,000 by FY30, because banks increasingly prefer to hand the low-margin grind of running machines to specialists like CMS.

So the honest framing is not collapse, it is a slow structural headwind on one leg of the business, against which CMS is racing to grow the other two legs. The managed services and technology layers grow as banks outsource more, regardless of whether cash is rising or flat. The question that decides everything is the pace of that internal mix shift.

3. The moat

CMS has a real but moderate moat. Scale is the first piece: the largest cash network in the country, with national reach that a new entrant cannot replicate cheaply. The second is switching cost: once a bank outsources its entire ATM operation, including cash forecasting, uptime and compliance, ripping that out is painful and risky, so contracts are sticky and long dated. The third, and the most interesting, is the technology layer. HAWKAI and the AIoT monitoring stack make the overall platform harder to displace and shift the revenue toward higher margin, recurring streams.

What CMS does not have is pricing power on the cash logistics leg, which is competitive and partly a pass-through of fuel and wages. So I read the moat as narrow on the legacy business and widening on the technology business. The direction of travel matters more than the current width.

4. Management and capital allocation

The company is led by Rajiv Kaul, Executive Vice Chairman and CEO, who has run CMS through its transformation from a pure cash business toward a platform. The capital allocation record is shareholder friendly in a way that is rare for a small cap. In FY26, a difficult year, the company still declared a total dividend of 5.25 rupees per share and approved a buyback of about 168 crore, repurchasing roughly 3 percent of equity at 340 rupees a share. A buyback at a price above the current market, funded from internal cash with no debt added, is management putting money where its mouth is on valuation.

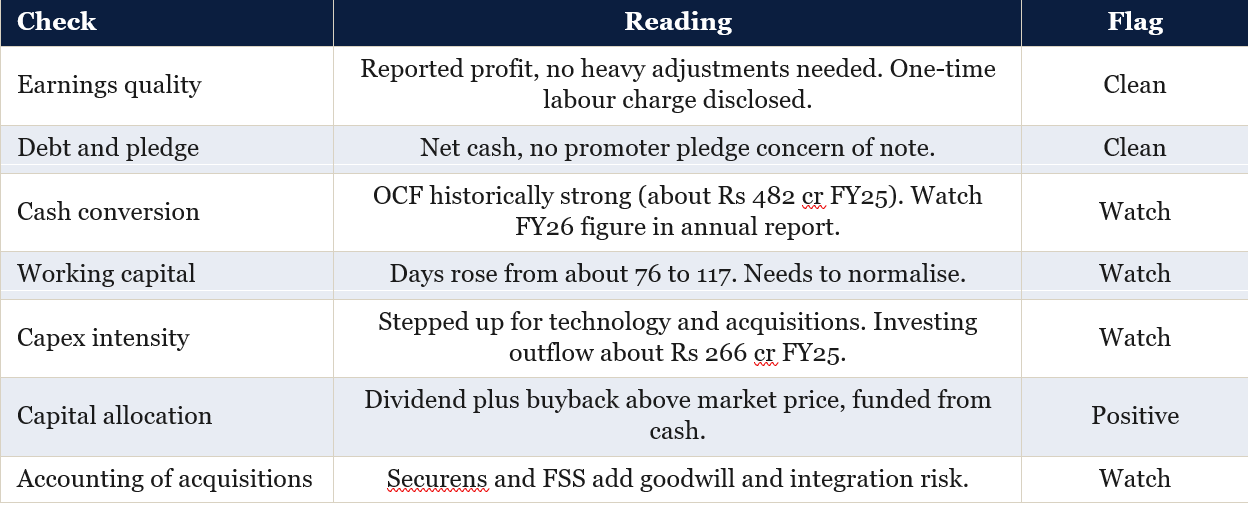

Two acquisitions tell you the strategic direction. Securens, a Vision AI business, was bought to scale the monitoring platform, and the FSS ATM managed services business was acquired in March 2026 for about 115 crore, adding around 8,000 ATMs and new bank relationships. Both push the mix toward managed and technology revenue, which is the stated plan.

5. The financials, including the bad year

I will not soften FY26. It was a poor year, and the cheap valuation exists because of it, not despite it. Revenue grew only 2.6 percent to 2,487 crore, and net profit fell about 18 percent to roughly 303 crore. Three things hit at once: a delayed SBI cash outsourcing project that management pegged at around 150 crore of lost revenue, a contraction in the off-site ATM market, and larger than usual wage hikes including a one-time labour code charge. Operating margins drifted from around 28 percent a few years ago to about 24 percent.

Reported history and segment mix

The recovery showed up in the fourth quarter. Q4 FY26 net profit rose 38 percent sequentially to about 79 crore, operating margin expanded 280 basis points to roughly 25.6 percent, beating the company’s own guidance, and services revenue crossed 600 crore for the first time. Management had called Q3 the bottom, and Q4 was the first quarter that looked like a turn rather than a hope.

Cash flow and balance sheet

The balance sheet is the quiet strength. CMS is effectively net cash. Operating cash flow was about 482 crore in FY25, up from 439 crore in FY24, so the business converts profit into cash well. The one watch item is working capital, where days stretched from about 76 to about 117 over the year, partly from the contract transitions and acquisitions, and capex stepped up to fund the technology build. These need to normalise, and I flag them openly rather than wave them away.

6. Forensic and quality checklist

7. Valuation, with the model shown

I value CMS two ways and then triangulate. First a discounted cash flow on the whole business, then a simple multiple cross-check, because no single method should be trusted alone on a company in transition.

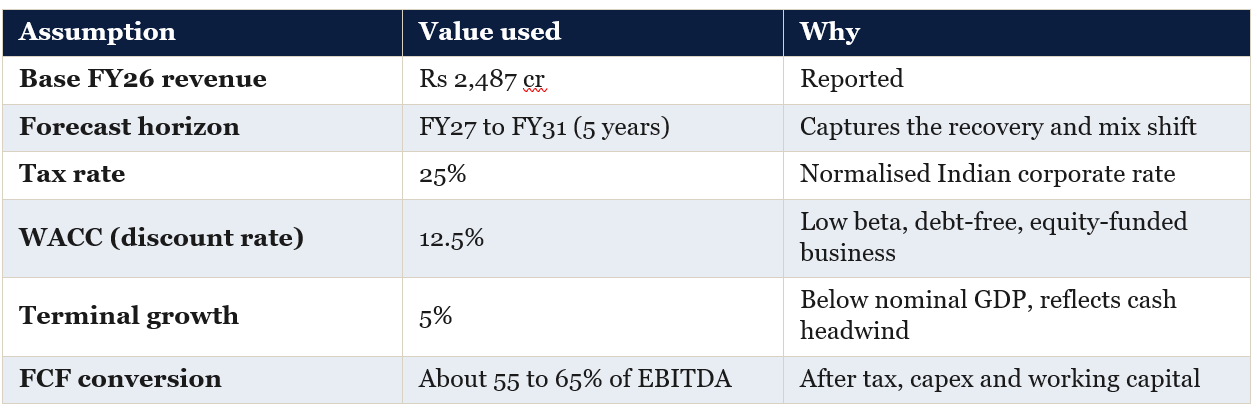

Discounted cash flow: shared assumptions

These are the inputs I have used. Change any of them and the answer changes, which is the point of showing them.

Three scenarios

The variables that actually swing the value are revenue growth and the EBITDA margin, because this is an operating-leverage business. I model three honest paths.

Discounting the free cash flows and a terminal value at 12.5 percent, then dividing by roughly 16.4 crore shares, gives the equity value per share below. I have rounded throughout, since false precision on a five year forecast helps nobody.

Probability weighting these (30 / 50 / 20) gives a discounted cash flow fair value of about 435 rupees per share. Against a reference price near 290 to 310, the model implies the market is pricing close to the bear case.

Multiple cross-check

The cross-check agrees, which gives me more confidence in the range than either method alone. On the base case, FY27 earnings of roughly 360 to 380 crore on about 16.4 crore shares is an EPS near 22 to 23 rupees. A peer-style multiple of 18 to 20 times, which is below the historical average CMS used to command and in line with one sell-side house’s 18 times target, points to a value of roughly 400 to 460 rupees. Both methods land in the low-to-mid 400s, well above the current price.

So both the cash flow model and the multiple approach converge around the low-to-mid 400s, while the stock trades near 300. The model’s message is simply that the current price embeds something close to the bear scenario.

8. What the analysis shows, and what it does not

Here is the honest summary, stated as findings rather than a recommendation, because this is education and the decision is yours.

— The facts: a debt-free market leader, around 18 percent return on capital, that just won mandates at India’s three largest banks, trading at a PE of roughly 13 against a peer median above 21 and below its own history.

— The catalyst: management states these three bank wins cover close to 85 percent of next year’s revenue, giving unusual visibility after a weak year.

— The model: a probability-weighted discounted cash flow fair value near 435 rupees, cross-checked by a multiple approach in the low-to-mid 400s, against a market price near 300.

— The catch: the cheap multiple is the price of a genuinely poor FY26, the cash leg faces a slow structural headwind, and the entire FY27 recovery rests on the SBI ramp delivering and margins reverting.

In other words, the model says the market is pricing CMS as a declining cash company, while the company is trying to prove it is a technology platform that the biggest banks in India just chose to trust. Which of those two is correct will be visible in three numbers over the next few quarters: whether the Q4 margin recovery holds, whether the SBI ramp shows up in reported revenue, and whether technology keeps climbing past 16 percent of the mix. I am presenting the work. What you do with it is entirely your call.

Five-line summary of the work

CMS Info Systems is a debt-free, cash-generative market leader in cash logistics that is deliberately shifting toward higher-margin managed services and AI-led technology. FY26 was a weak year, with profit down about 18 percent on flat revenue, driven by an SBI project delay, an off-site ATM contraction and wage inflation, which is why the stock fell about 35 percent. The fourth quarter showed a clear sequential recovery, and management says the new SBI, ICICI and HDFC mandates already cover close to 85 percent of FY27 revenue. My three-scenario discounted cash flow, with all assumptions shown, produces a probability-weighted fair value near 435 rupees, and an independent multiple cross-check lands in the same low-to-mid 400s, while the stock trades near 300. The analysis shows the current price embeds close to the bear case, but the outcome depends entirely on whether the margin recovery and the SBI ramp actually materialise, and none of this is a recommendation to act.

Disclaimer

I am not a SEBI registered investment adviser or research analyst. This document is my personal research, prepared and shared purely for educational and informational purposes. It is not investment advice, not a recommendation, and not an offer or solicitation to buy or sell any security. It contains no buy, sell or hold call by design. I hold the NISM Series XV (Research Analyst) certification, but that does not make this advice. Every figure is drawn from public sources, including company filings, the Q4 and FY26 results, the earnings call, broker material and Screener, and while I have made every effort to be accurate, figures can contain errors or change after publication, and several items remain to be confirmed against the full annual report. The discounted cash flow and all projections are illustrative models built on assumptions that are explicitly stated and that will not match reality. I may hold or transact in the security discussed. Markets carry real risk and you can lose money. Please do your own research and consult a SEBI registered adviser before making any investment decision.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.