ESSAY

Gaudium IVF and Women Health Ltd

14 May 2026

Important note before you read: Gaudium IVF listed on February 27, 2026. This is a very recently listed, small company with limited price history, thin liquidity, and several known risks. This report is written for investors with a 3 to 5 year horizon who understand small cap risk. Read the full risk section before forming any view.

1. Why I Am Writing About This Company

I want to be upfront about something. I am not writing this because the stock has already run up and I want to chase momentum. I am writing this because one of India’s most respected investors, Mukul Mahavir Agrawal, deployed Rs 29 crore of capital into this company in the March quarter 2026, just weeks after it listed. That is not a casual bet. His portfolio runs over Rs 7,130 crore across 74 stocks. When someone like that enters a company this small this quickly after its IPO, it is worth understanding why.

The company is Gaudium IVF and Women Health. India’s first and only listed pure-play fertility clinic company. It listed on February 27, 2026. Mukul Agrawal built a 1.02% stake, comprising 44.44 lakh shares, through open market purchases between March 13 and March 31. He had zero prior exposure to this company before that. This was not a pre-IPO anchor entry. He watched it list, saw what he needed to see, and bought.

This report is my attempt to understand what he saw. And to figure out whether the stock at current levels is worth owning for the next three to five years.

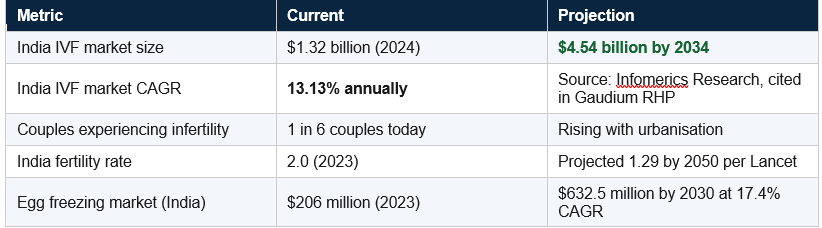

One data point before we get into the numbers. One in six couples in India are currently experiencing infertility according to Nova IVF CEO Shobhit Agarwal, speaking to Business Standard in June 2025. That is approximately 27.5 million married couples actively trying to conceive, per Dr. Ajay Murdia of Indira IVF. And right now, there is exactly one listed company in India that is a pure play on solving this problem.

2. The Business

What Gaudium Actually Does

Gaudium IVF was founded in 2015 by Dr. Manika Khanna in Delhi. Dr. Khanna is a fertility specialist with over 25 years of clinical experience. She built the company from a single clinic in Janakpuri, West Delhi, into a network that today spans 35 locations across India.

The core business is IVF treatment. In vitro fertilization is a process where eggs are retrieved from a woman, fertilised with sperm in a lab, and the resulting embryo is transferred back into the uterus. It is a deeply specialized medical procedure requiring embryologists, fertility specialists, a fully equipped lab, and precise clinical protocols. The process costs anywhere from Rs 1.5 lakh to Rs 4 lakh per cycle in India. Gaudium’s average revenue per patient stood at Rs 3.55 lakh in FY25.

Beyond IVF, the company also does IUI, ICSI, ovulation induction, egg freezing, male infertility treatment, PCOS management, and surrogacy-related services. IVF and related treatments contribute approximately 79% of total revenue. The remaining 21% comes from hospital services from its 15-bed day-care hospital in Janakpuri and an in-house pharmacy through its subsidiary Gaudium International.

The Hub and Spoke Model

This is the most important structural thing to understand about the business. Gaudium does not replicate a full lab at every location. That would be expensive, slow to set up, and hard to staff. Instead, it operates seven full hubs, which are complete IVF centres with embryology labs, operating theatres, and senior specialists. Then it runs 28 smaller spoke clinics that do consultations, diagnostics, and initial patient work. Complex procedures funnel back to the nearest hub.

This structure lets Gaudium expand geographically without duplicating the most capital-intensive parts of the operation at every location. A spoke clinic can be set up for a fraction of what a full hub costs. It also lets the company reach tier-2 cities where patient demand exists but full IVF centre economics may not yet justify a hub investment.

With IPO proceeds, the company plans to open 19 new full IVF hubs at an average cost of Rs 2.6 crore each, funded by Rs 50 crore from the fresh issue. This will take the hub count from 7 to 26 by FY29, more than tripling the full-scale clinical footprint.

Clinical Performance

In fertility medicine, the success rate is the single most important metric. It drives word of mouth. It drives referrals. It builds or destroys brand reputation. Gaudium reports a clinical success rate of 58.74% per IVF cycle. The industry average in India is 40 to 45%. So Gaudium is meaningfully above the average.

However, there is a notable gap versus some peers. Inspire IVF, a listed Thai company, reports success rates above 70%. This gap is worth monitoring as Gaudium expands into new geographies where its brand is less established and where maintaining lab quality standards across new hubs will be genuinely difficult.

3. The Industry Backdrop

Why This Problem is Getting Bigger, Not Smaller

India’s total fertility rate, meaning the average number of children a woman will have in her lifetime, has fallen from 3.1 in 2003 to 2.0 in 2023. It is projected to fall further to 1.29 by 2050, well below the replacement level of 2.1 per woman per generation. This is primarily driven by delayed marriages, higher female workforce participation, urban stress, lifestyle changes, and rising rates of conditions like PCOS, which affects up to 22.5% of Indian women.

The irony is powerful. India has the world’s largest population and is simultaneously facing a growing infertility crisis. Delayed marriage means women are trying to conceive in their mid to late 30s instead of their mid-20s. Fertility declines sharply with age. The result is a growing structural gap between the desire to have children and the biological ability to do so naturally.

This is not a trend that reverses. It compounds. Every year that urbanisation deepens, that career timelines extend, and that stress levels in Indian cities remain where they are, the addressable patient pool for IVF grows larger.

The Market Numbers

Regulation is Actually a Tailwind Here

This is a part of the story that gets underappreciated. India passed the Assisted Reproductive Technology Regulation Act in 2021 and the Surrogacy Regulation Act in 2021. Commercial surrogacy has been banned. Embryo trading is prohibited. Sex selection is banned. These laws effectively closed down a large number of unregulated small clinics that were operating in the grey zone.

What this means for an organised, compliant, listed player like Gaudium is that the competitive landscape is being cleansed of fly-by-night operators. Patients who previously might have gone to an uncertified local clinic are increasingly seeking out regulated, quality-assured chains. The regulatory tightening benefits the organised players disproportionately. This is the same dynamic that played out in banking after post-2012 NPA recognition, or in diagnostics after NABL accreditation became the norm.

4. The Moat

IVF is not a commodity business. You cannot build a good IVF clinic the way you open a pharmacy. The moat here is built from three sources, and it is important to understand each one clearly.

Source 1: Clinical Outcomes and Brand Trust

In IVF, outcomes are everything. A patient making a decision about which clinic to visit for something as emotionally loaded as fertility treatment does not choose based on price alone. They ask: what is your success rate? They talk to friends who have been through it. They read reviews. They ask their gynaecologist for a referral.

Gaudium’s 58.74% success rate is above the 40 to 45% industry average. This creates a self-reinforcing loop. Better outcomes drive more referrals. More referrals drive more volume. More volume drives more clinical experience and better training. This brand moat takes years to build and cannot be replicated quickly by a new entrant writing a large cheque.

Source 2: The Regulatory Compliance Barrier

Running an IVF clinic in India today requires registration under the ART Act, adherence to ICMR guidelines, NABL-accredited labs, qualified embryologists, and strict record-keeping. For a new entrant, navigating these requirements is expensive and time-consuming. For Gaudium, which has been building its compliance infrastructure since 2015, this is already done and forms part of its cost base. New competition has to climb the same wall from scratch.

Source 3: Specialist Talent Dependency

This one cuts both ways. Gaudium’s clinical quality depends entirely on the quality of its embryologists and senior fertility specialists. Retaining this talent is one of the company’s most important competitive activities. Currently the company runs on just 5 core embryologists for the entire business. That is simultaneously a moat because replacing experienced embryologists is hard, and a risk because losing even one creates a capability gap.

Moat verdict: Narrow but real. The clinical brand, regulatory compliance infrastructure, and specialist talent combine to create meaningful barriers to fast replication. The moat is not wide enough to guarantee pricing power forever. But it is wide enough to protect market position in established geographies for at least 5 to 7 years if execution remains strong.

5. Management and Founders

Dr. Manika Khanna

Dr. Khanna is the founder, promoter, and Managing Director. She started Gaudium in 2015 with a single clinic in Janakpuri. She has built it over 11 years into a 35-location network with Rs 71 crore in revenue in FY25. A clinician who has turned into an operator while maintaining clinical credibility is rare. Most clinic founders either stay in the lab and never build the institution, or step back from clinical work to manage the business. Dr. Khanna has done both simultaneously.

Her promoter stake was reduced from 99.32% pre-IPO to 70.73% post-IPO as part of the OFS component. The OFS raised Rs 75 crore. At her IPO price, she monetised a meaningful portion of her holding, which is normal for a founder after 11 years of building. Post-IPO she still holds over 70% of the company, which is a strong alignment signal.

The one governance item to flag: Dr. Khanna has personally undertaken to cover the Rs 44 crore tax contingent liability through unsecured debt or equity if it materialises and the company cannot meet it. That is a positive commitment but it also tells you she is aware this liability is real and material enough to require a personal guarantee.

Capital Allocation

The IPO proceeds breakdown was clean. Rs 50 crore for setting up 19 new IVF hubs. Rs 20 crore for debt repayment. Balance for general corporate purposes. This is not complicated. The company is doing exactly what it said it would do at IPO with the capital it raised.

The one tension worth flagging is philosophical. Gaudium’s entire brand narrative at IPO was built around an asset-light hub-and-spoke model. Yet the expansion plan involves 19 new full IVF hubs, each requiring a fully equipped embryology lab. These are not asset-light investments. They are capital-intensive fixed assets that take 12 to 18 months to reach breakeven. The company is essentially betting that it can maintain its financial profile while simultaneously tripling its most capital-intensive asset class. That is a reasonable bet but it is a bet, not a certainty.

Capital allocation grade: B. The IPO use of funds is sensible. The founder’s personal commitment on the tax liability shows skin in the game. The hub-vs-asset-light tension needs watching. Grade improves to B+ if the first two or three new hubs hit breakeven within 18 months of opening.

6. Financial Analysis

The Revenue Trajectory

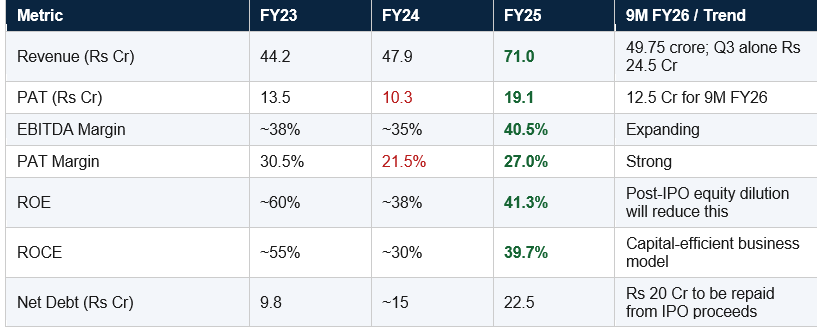

Gaudium’s revenue growth story is genuinely impressive for a company of this size and age. From Rs 44 crore in FY23 to Rs 71 crore in FY25 is a 27% two-year CAGR. And then in the first three quarters of FY26 alone, the company has already done Rs 50 crore in revenue, running at an annualised rate of approximately Rs 95 to 100 crore. The Q3 FY26 standalone quarter showed revenue of Rs 24.5 crore against Rs 14.4 crore in Q3 FY25, which is 70% year-on-year growth in a single quarter.

Sources: Gaudium IVF RHP filed with SEBI, BSE filings, PL Capital IPO review, BusinessToday.

FY24 PAT Dip: What Happened

This is worth explaining because a PAT decline from Rs 13.5 crore in FY23 to Rs 10.3 crore in FY24 looks bad on the surface. The answer is expansion-related costs. The company was opening new locations and hiring ahead of revenue in FY24. When you open new IVF hubs, they take 12 to 18 months to reach breakeven. The cost of running a new hub hits the P&L immediately, but the revenue ramp takes time. The FY24 dip was a deliberate investment in growth infrastructure, not a deterioration in the core business. FY25 confirmed this with PAT rebounding 85% to Rs 19.1 crore. The same dynamic will likely play out as the 19 new hubs open over FY27 to FY29.

The Two Red Flags in the Financials

I want to be direct about two numbers that I think every investor in this company needs to watch closely.

First, debtor days are at 170 days per Screener data. For a business that is essentially a pay-before-procedure healthcare model, this is high. It likely reflects the hospital services segment and some corporate/insurance billing cycles. But it needs to come down as scale increases. High receivables in a small company are a cash flow risk.

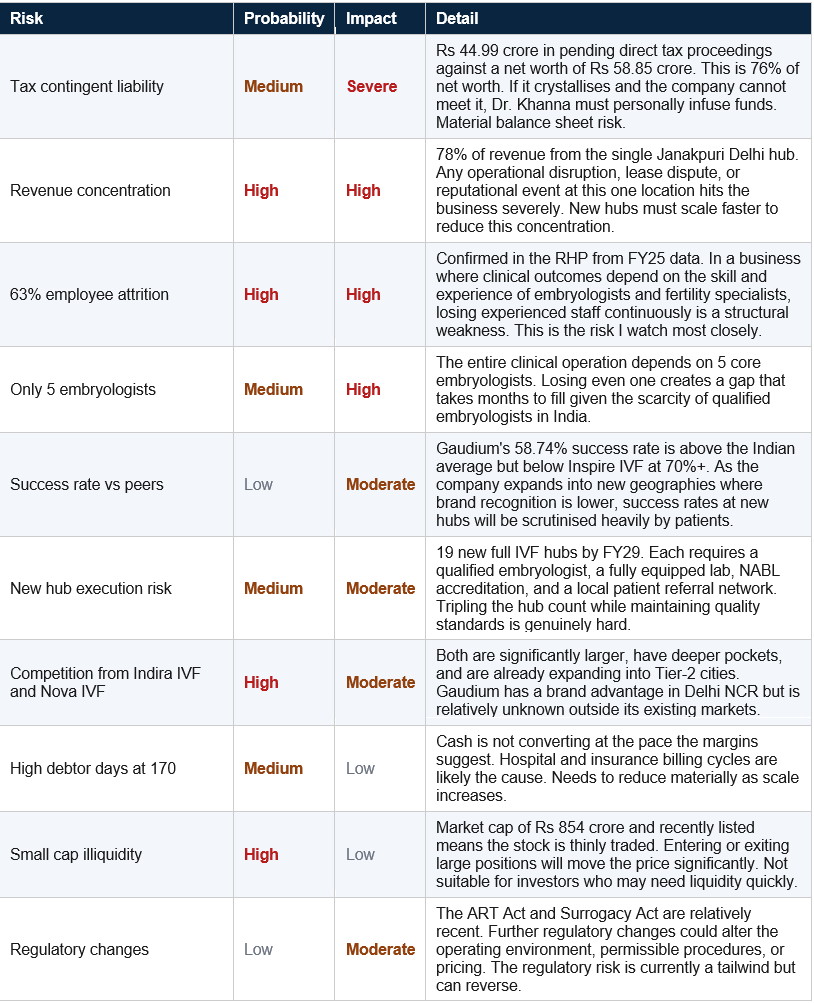

Second, the contingent liability of Rs 44.99 crore as of September 2025 represents 76% of the company’s net worth of Rs 58.85 crore. This is a direct tax proceeding. If this liability crystallises, the impact on the balance sheet would be significant. Dr. Khanna’s personal guarantee provides comfort but is not a clean solution. This overhang needs to be resolved before the company can trade at a premium valuation with confidence.

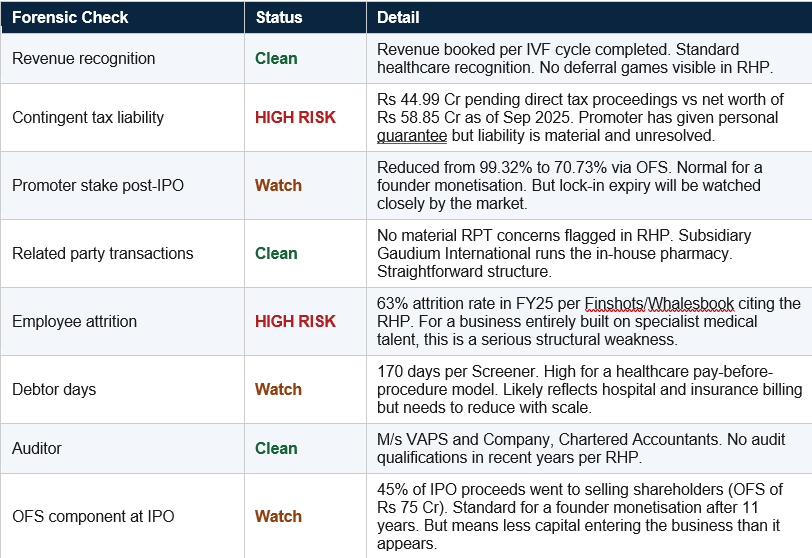

7. Forensic Checks

Forensic verdict: The business is clean on revenue recognition and audit quality. The two genuine concerns are the tax contingent liability which is disproportionately large relative to net worth, and the 63% employee attrition which is a systemic risk for a talent-dependent business. Both need resolution before a high-conviction position can be built.

8. Valuation

How to Think About Valuing This

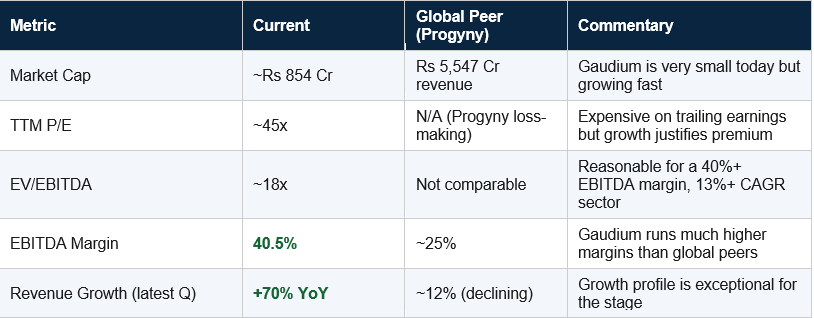

Gaudium is a small, recently listed, high-growth healthcare company in a sector with no direct Indian listed peer for comparison. Traditional P/E multiples are less useful here because earnings are still small enough that they will move significantly as new hubs open and ramp up. The three frameworks I use are EV to EBITDA, EV to revenue, and a forward earnings model based on the hub expansion.

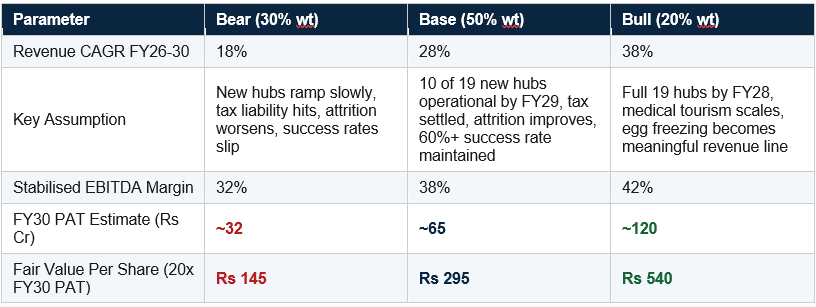

Scenario Analysis

Probability-weighted fair value: 30% x 145 + 50% x 295 + 20% x 540 = Rs 43.5 + Rs 147.5 + Rs 108 = Rs 299 per share.

At the current CMP of approximately Rs 380, the stock is trading at a 27% premium to my probability-weighted fair value of Rs 299. The stock is not cheap today. However the base case target of Rs 295 and the bull case of Rs 540 illustrate the optionality that exists if the hub expansion executes well. The entry zone of Rs 300 to Rs 340 represents a 12 to 25% discount to fair value, which is the minimum margin of safety I want before building a position in a company this small with this many execution dependencies.

A 20x FY30 PAT multiple is conservative for a high-quality healthcare compounder in India. Apollo Hospitals, Narayana Health, and Dr Lal PathLabs all trade at 30 to 50x earnings. If Gaudium maintains 40%+ EBITDA margins and 25 to 30% growth through FY30, re-rating to 25 to 30x is not unreasonable, which makes the bull case more accessible than the bear case.

9. Full Risk Register

DISCLAIMER

This research report has been prepared by Compound with Raunak for educational and informational purposes only. It does not constitute investment advice, a solicitation, or an offer to buy or sell any security. The author is not a SEBI registered investment advisor. All financial data, estimates, and projections contained in this report are sourced from publicly available information including Gaudium IVF’s Red Herring Prospectus filed with SEBI, BSE filings, analyst reports from PL Capital, Swastika Investmart, Arihant Capital, and SMIFS, and financial media including BusinessToday, Business Standard, and Finshots. While reasonable care has been taken to ensure accuracy, no guarantee is made regarding completeness or accuracy. Past performance of any security does not guarantee future results. Investing in equity markets involves significant risk, including the possible loss of your entire principal. Gaudium IVF is specifically flagged as a high-risk small cap investment. Readers must conduct their own due diligence and consult a SEBI registered financial advisor before making any investment decisions. The author may or may not hold positions in the securities discussed. This report reflects information available as of May 2026.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.