ESSAY

Goodluck India Limited

5 June 2026

Why I pulled this one apart

Defence stocks are the easiest thing to hype right now, and the hardest to do honestly. So when I saw Goodluck India making headlines for an artillery shell order, my first instinct was to be skeptical, not excited. A steel pipe company suddenly making weapons sounds like a story written for the algorithm. But I opened the filings, and what I found is more interesting than the headline. This is a profitable, dividend paying engineering company that has quietly built a real, licensed capability in 155mm artillery shells, right as the world cannot make enough of them. That combination is rare. It is also not without risk, and I will be blunt about where the risk sits.

One thing up front. I am not a SEBI registered Research Analyst yet, that registration is in process. So there is no buy, sell, or recommendation anywhere in this note. You did ask for the valuation, so I have shown the output of every model I ran, with the assumptions in the open. Treat those as illustration of how the business could be valued under different assumptions, not as a target or as advice.

Stage 1. Understanding the business

Goodluck India, established in 1986 and based near Ghaziabad in Uttar Pradesh, is a diversified engineering and steel products company. It is not a defence pure play, and it is important to start there. The bulk of its revenue comes from four traditional verticals: engineering structures and fabrication for railways, highways, power and solar, precision pipes and auto tubes, cold rolled sheets and hollow sections, and a forgings division. It is a real, cash generating, mid sized manufacturer with a long operating history.

The new chapter is Goodluck Defence and Aerospace Limited, the subsidiary launched in August 2023. This is where the artillery shell story lives. The forgings heritage matters here, because Goodluck has supplied components into defence and space programs including DRDO, ISRO, HAL and BrahMos through that division for years. The 155mm shell business is an extension of metallurgy and forging skills the company already had, not a leap into the unknown. That is the single most important thing to understand about why this is credible and not just a press release.

The one nuance that keeps you honest

Goodluck makes the shell in Ready to Fill condition. That means the metal shell body, not the explosive filling, which is done separately by government ordnance factories. So this is high precision metal manufacturing inside the ammunition supply chain, not a weapons or explosives maker. Get this right and no one can catch you out.

Stage 2. Industry and macro backdrop

The tailwind is genuine and global. Since 2022, the world has been short of 155mm artillery shells, the standard heavy calibre round. Western producers have spent two years trying to catch up and are still behind their own targets. United States output has run near 40,000 rounds a month against a 100,000 target that keeps slipping, and Europe has been racing to roughly double its annual capacity. When the established defence industrial bases of the West cannot keep up, the supply chain widens to qualified manufacturers elsewhere. India is one of those places.

Layer on the domestic policy push. India wants to move from being one of the world’s largest arms importers to a top tier defence exporter, and Atmanirbhar Bharat has actively pulled private companies into ammunition, an area once reserved for state owned ordnance factories. Several private names are now entering 155mm production, including much larger groups. So the opportunity is real, but Goodluck is competing for it, not alone in it. I would never frame this as the only player, because it is not.

Stage 3. The moat

The core engineering business has a modest moat at best. Steel pipes, tubes and structures are competitive, capital intensive and partly commoditised, which is exactly why the blended margins sit around 10 percent. I do not pretend otherwise.

The defence arm is where a narrower but more durable moat is forming, built on three things.

1. Licensing and qualification. An industrial licence to make 105mm to 155mm shells, plus the testing and certification to export them, takes years and is a real barrier. Goodluck has cleared it and shipped abroad, which most aspirants never reach.

2. Metallurgy and forging heritage. The forging skills behind defence and space components are not easily replicated, and they shorten the path to credible shell manufacturing.

3. Approved vendor status. Once qualified for an artillery programme, repeat and follow on orders tend to favour the incumbent, which is the annuity that makes this attractive if it scales.

Stage 4. Management and ownership

Goodluck is promoter run, with promoter holding around 56.4 percent, an unmodified audit opinion for FY26, and a track record of paying dividends, with a ₹3 per share final dividend recommended for the year. I read the capital allocation as deliberate and growth oriented. The company put through heavy capital expenditure in FY25, with investing outflows of roughly ₹473 crore, to build the defence facility in Sikandrabad and expand the core. That is the right kind of spending if the orders follow, and the early defence orders suggest the thesis is being validated. The flip side is that this spending has raised debt, which I cover in the financials.

Management has stated a clear ambition for the defence arm: to reach around 10 percent of total revenue within three to four years, implying roughly ₹350 to 400 crore of defence revenue at full capacity, at margins above the group average. That is the number to hold them to.

Stage 5. The financials

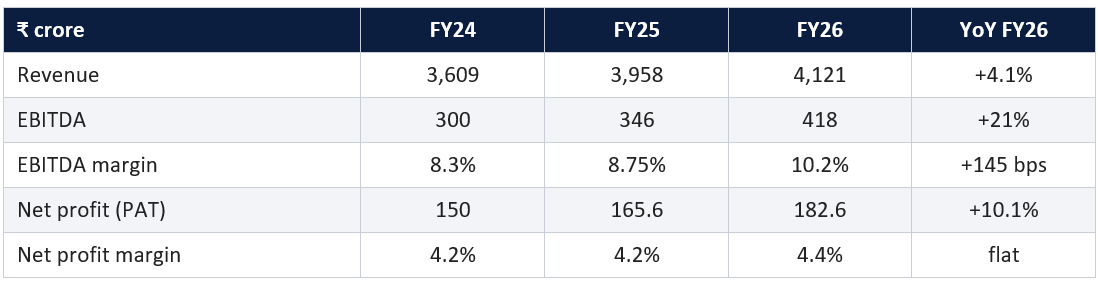

Here is the three year shape of the business.

What the numbers actually say

Two honest reads sit side by side. The good: profit grew faster than revenue because margins expanded meaningfully, the fourth quarter was a record, and the defence orders have started landing. The sober: revenue grew only about 4 percent, so this is not yet a fast growing company, and the net margin is a thin 4 percent, which is normal for steel led engineering. The excitement is entirely about what the defence mix does to that margin over time, not about the base business suddenly accelerating.

Balance sheet and returns

This is where caution earns its place. Borrowings rose to roughly ₹1,079 crore from about ₹882 crore as the company funded expansion, putting debt to EBITDA near 2.9 times. That is manageable for a profitable manufacturer, but it is not a debt light balance sheet, and during a heavy capex phase free cash flow is under pressure. Returns are moderate: ROCE around 12.5 percent and ROE around 12 to 13 percent. Respectable for diversified engineering, not the mark of a high return compounder. For the stock to re rate durably, those returns need to climb as the higher margin defence revenue scales. That is an output to watch, not an assumption to bank.

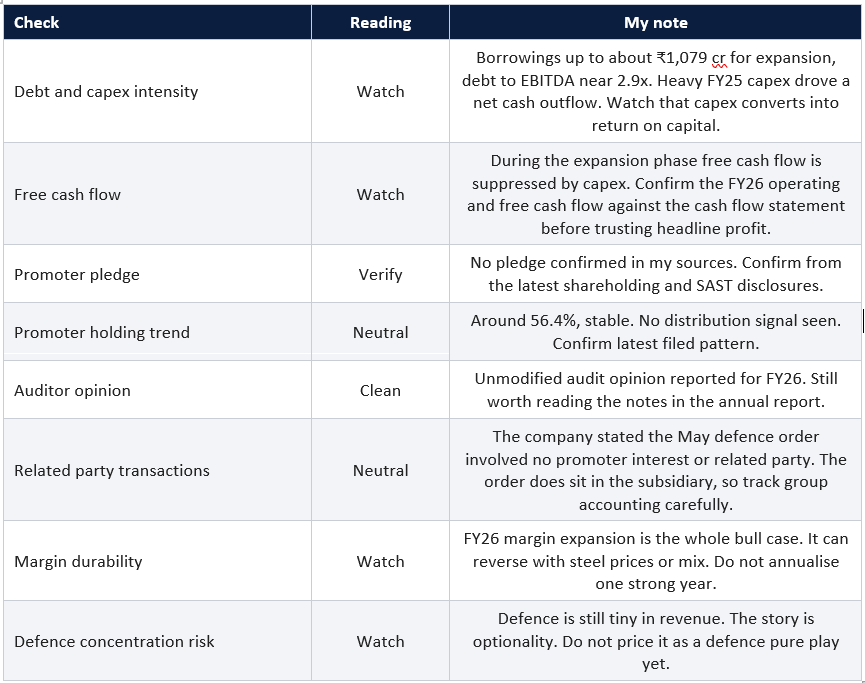

Stage 6. Forensic red flag checklist

I run this on every company. Here is the honest scorecard.

Data gaps I am openly flagging

Before acting, I would confirm three things from primary filings: the exact FY26 operating and free cash flow, any promoter pledge, and the precise current share count and net debt, because the per share valuation below moves with the last two. Flagging gaps beats guessing past them.

Stage 7. Valuation, every model

You asked for the valuation under all the models, so here it is in full. Read this as illustration, not instruction. Each model takes a different lens, and the spread between them is itself the message. None of this is a price target or a recommendation.

Assumptions I am working from

Shares outstanding about 2.93 crore, net debt about ₹950 cr, FY26 PAT ₹182.6 cr, FY26 EBITDA ₹418 cr, current market price near ₹1,350 and market capitalisation near ₹3,950 cr. The per share figures below depend directly on the share count and net debt, so confirm both against the latest filing before you rely on any number.

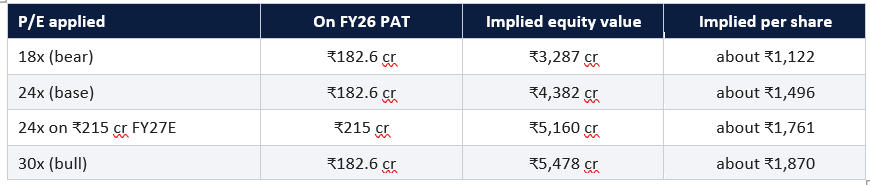

Model 1. Relative valuation on earnings

Diversified engineering companies tend to trade around 15 to 22 times earnings, while a credible defence angle can pull the multiple toward 28 to 35 times. Applying a band to FY26 profit of ₹182.6 cr gives the range below. I also show a base case forward profit of about ₹215 cr, assuming low double digit growth as defence contributes.

Model 2. EV to EBITDA

Engineering peers trade around 8 to 14 times EBITDA. Applying that to FY26 EBITDA of ₹418 cr, then subtracting net debt of about ₹950 cr, gives equity value.

Model 3. Discounted cash flow, three scenarios

A DCF here needs a health warning. Because the company is in a heavy capex phase, near term free cash flow is low or negative, so the value sits heavily in the later years and the terminal value. I used a five year explicit window, a discount rate near 12.5 percent and a terminal growth of about 4.5 percent. Treat the output as broad, not precise.

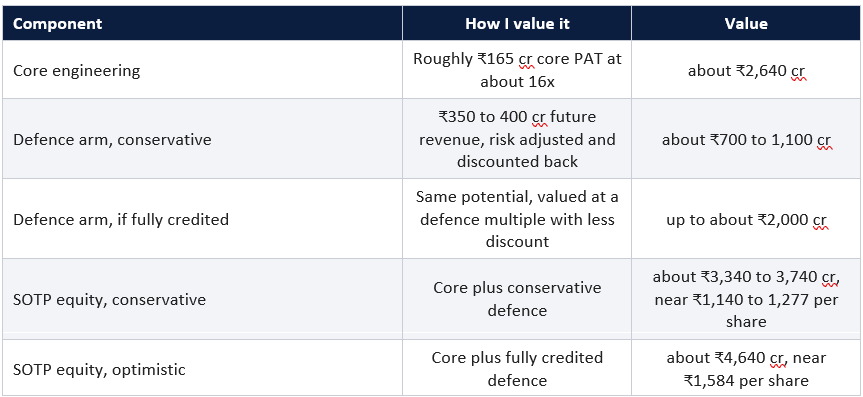

Model 4. Sum of the parts

This is the most natural lens for Goodluck, because the value is two different things bolted together. I value the core engineering business on a modest earnings multiple, then add the defence arm separately as a risk adjusted option on its stated potential.

Model 5. Reverse DCF, what the price already assumes

The most useful exercise of all. Instead of guessing the future, ask what the current price near ₹1,350 already demands. At that level and the current multiple, the market appears to be paying for the core business plus a partial success of the defence ramp. In other words, some of the artillery story is already in the price, but not the full bull case. That is the honest centre of gravity. If the defence arm scales to management’s 10 percent of revenue at strong margins, the upper models look reachable. If it stalls or stays tiny, the bear models are where gravity pulls.

Pulling the models together

Across all five lenses, the illustrative outputs cluster roughly between ₹1,050 at the cautious end and ₹2,100 at the optimistic end, with several models landing in a central band around ₹1,300 to ₹1,550. The current market price sits in the lower middle of that spread. What that means for you, whether the optionality is worth the price and the risk, is a personal judgement I cannot and will not make for you. The models are the map, not the decision.

The one line valuation summary

The core engineering business roughly supports the lower end of the range on its own. Everything above that is the market paying, partly, for the 155mm defence ramp to work. So this is, at heart, a priced bet on execution in the defence arm.

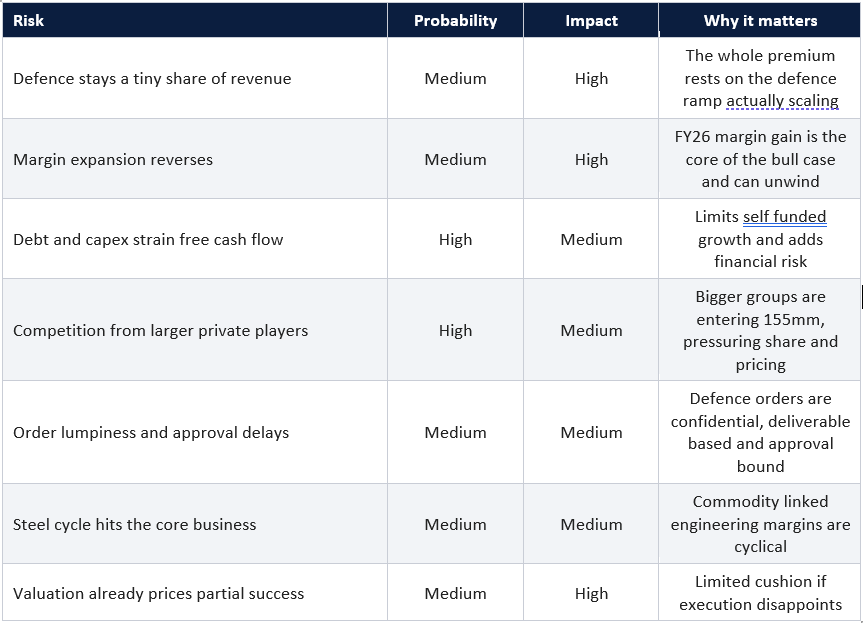

Stage 7b. Risk register

Probability and impact are my qualitative judgement, scored Low, Medium or High.

My five sentence summary

1. Goodluck India is a profitable, dividend paying, diversified engineering company that has built a credible, licensed capability in 155mm artillery shells through its subsidiary, just as the world faces a structural shortage of them.

2. FY26 was driven by margin expansion rather than growth, with revenue up only about 4 percent but profit up around 10 percent and a record fourth quarter.

3. The balance sheet carries more debt than I would like after a heavy capex cycle, and returns on capital are moderate at around 12 to 13 percent, so this is not yet a high return compounder.

4. Across every valuation model, the value splits cleanly into a core engineering business plus a risk adjusted option on the defence arm, and the current price appears to embed partial success of that defence ramp.

5. This is an execution story to watch and verify quarter by quarter, the defence revenue mix and the cash flow will tell you far more than any single order headline, and none of this is a recommendation to act.

What I will be tracking from here

• Defence revenue as a share of the total, against management’s 10 percent goal, and any new domestic or export orders for 155mm shells.

• Operating and free cash flow in the FY26 annual report, and whether debt to EBITDA starts falling as capex moderates.

• Whether the FY26 margin expansion holds in the coming quarters or fades with the steel cycle.

• Utilisation of the new defence facility as capacity ramps from 1.5 lakh toward 4 lakh shells a year.

• Competitive moves from the larger private players entering artillery ammunition, which could pressure Goodluck’s share of new orders.

Important disclaimer and disclosures

This note is published for educational and informational purposes only. It is my personal analysis and opinion, written under the Compound with Raunak banner.

I am not registered with the Securities and Exchange Board of India (SEBI) as a Research Analyst or as an Investment Adviser. Nothing in this document is investment advice, a research report as defined under the SEBI (Research Analysts) Regulations, or a recommendation, solicitation or offer to buy, sell or hold any security.

This note contains no buy, sell or hold call. The valuation models and the fair value ranges shown are illustrative analysis intended only to demonstrate how the business could be valued under different assumptions. They are not price targets, forecasts or guarantees, and they must not be read as advice or as a basis to trade.

All figures are sourced from publicly available exchange filings, company disclosures and reputable financial media, and were believed accurate as of 31 May 2026. Some figures are approximated or rounded and may have been revised. Always verify every number, especially the share count, net debt and cash flows, against the company’s primary filings before relying on it.

Securities markets carry risk and you can lose money, including your entire capital. Smaller companies and defence linked stocks can be especially volatile and illiquid. Past performance is not indicative of future results.

Disclosure of interest: I confirm my own position in Goodluck India Limited before publishing this note, and you should assume I may hold, may not hold, or may transact in the security. [Author to set the exact disclosure line here, for example: As of the date of publication, I do not hold any position in Goodluck India Limited.]

You are solely responsible for your own investment decisions. Please do your own research and consult a SEBI registered investment adviser who can take your personal financial situation into account before making any decision.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.