ESSAY

Sharda Cropchem Limited

7 April 2026

Why I Am Writing This

In the March 2026 quarterly shareholding filings, Rajiv Khanna - the Chennai-based investor who manages Dolly Khanna’s portfolio - re-entered Sharda Cropchem Limited, picking up approximately 9.8 lakh shares and securing a 1.09% stake. This is not a first entry. He held this stock previously at 1.38% in March 2022 and exited during the severe agrochemical downcycle of FY24. He watched the earnings collapse, waited, and came back.

That pattern- a studied exit followed by a deliberate re-entry after cycle confirmation - is worth paying attention to. This note explains what Sharda Cropchem does, why the business is structurally different from most agrochemical names, what the numbers look like today, and what the risks are.

Understanding the Business Model

Most investors look at Sharda Cropchem and see an agrochemical exporter. That is technically correct but fundamentally incomplete. The better mental model is this: Sharda is an IP and regulatory platform that happens to sell agrochemicals.

Here is how the model actually works. Sharda identifies generic agrochemical molecules — molecules whose original patents have expired — across the fungicide, herbicide, and insecticide categories. They then build detailed regulatory dossiers for those molecules and file for product registrations in tightly regulated markets: the European Union, the NAFTA region (USA, Canada, Mexico), and Latin America. Once a registration is granted in their name, they have the legal right to sell that product in that market. They then outsource the actual manufacturing entirely to third-party Chinese suppliers, take delivery, and distribute.

There is no factory on their balance sheet. No manufacturing risk. No capex on production assets. The entire competitive advantage is the registration portfolio — a collection of regulatory approvals that took years to obtain and cannot be copied quickly.

The Registration Moat

Getting a single product registration approved in the EU takes 5 to 8 years and costs crores per application. The process involves assembling toxicology data, environmental impact assessments, efficacy studies, and regulatory dossiers for submission to national competent authorities across member states. It is expensive, time-consuming, and requires specialist regulatory knowledge built over decades.

As of Q3 FY26, Sharda has:

• 2,994 active product registrations globally

• 1,076 applications currently at various stages of the approval pipeline

• Presence across 80+ countries in Europe, NAFTA, and LATAM

• ₹500 crore of planned annual capex dedicated entirely to new registration filings in FY26

A competitor starting from zero today would need decades and thousands of crores to build a comparable portfolio — and the clock starts from nothing. This is a real, durable entry barrier. Not a story, not a management narrative. A quantifiable structural moat.

The Cycle That Created the Opportunity

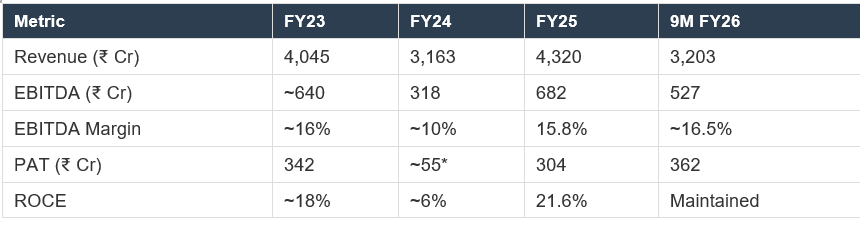

To understand why this re-entry matters, you need to understand what happened to Sharda in FY24. After strong FY23 revenues of ₹4,045 crore and PAT of ₹342 crore, the global agrochemical sector entered a brutal inventory destocking cycle. European and North American distributors had built excess inventory during the COVID supply-chain boom. When demand normalised, they stopped buying and worked down their stockpiles.

For Sharda, the impact was swift and severe. Revenue fell to ₹3,163 crore in FY24 — a 22% decline. EBITDA was cut by more than half, collapsing from ~₹640 crore to ₹318 crore. PAT fell by over 80% in a single year. The stock followed.

This is the context in which Dolly Khanna exited. Not because the business was broken - the registrations were still there, the model was still intact — but because the earnings cycle had turned against them and the stock had no near-term catalyst. Exiting a structurally sound business in a down-cycle is not a loss of conviction. It is capital allocation discipline.

The Recovery: What the Numbers Say Now

The recovery that began in FY25 has accelerated sharply in FY26. Here is the progression:

The headline number that stands out: the company achieved its highest-ever annual PAT within the first nine months of FY26 alone — ₹362 crore in 9M FY26, already exceeding full-year FY25’s ₹304 crore. On a trailing twelve month basis, revenue stands at ₹5,031 crore and net profit at ₹566 crore.

Q3 FY26 was particularly strong: revenue grew 39% year-on-year to ₹1,289 crore, while PAT jumped 366% year-on-year to ₹145 crore. Fungicides led growth with a 71% year-on-year increase. Europe — their largest market — more than doubled agrochemical revenues in Q3 alone.

Gross margins have also structurally improved: from 25.9% in FY24 to 29.8% in FY25 and 34.9% in Q3 FY26. Management has guided for FY26 EBITDA margins in the 18–20% range, and FY27 revenue growth of 15–20%.

Balance Sheet: A Clean Foundation

What makes this recovery more credible is what is underneath it:

• Completely debt-free

• ₹826 crore in cash, bank balances, and liquid investments as of December 2025

• Promoter holding: 74.8% — no pledging disclosed

• No off-balance-sheet liabilities or SPV structures flagged

• Operating cash flow has consistently exceeded net income — a clean earnings quality signal

The Bubna family has run this business since 1987. The Chairman and MD, Ramprakash Bubna, has built the registration model systematically over three decades. 74.8% promoter holding with zero pledging in a small-cap environment is a meaningful governance signal.

Valuation: What Are You Paying For?

At a CMP of approximately ₹880–906, the stock trades at roughly 14–16x TTM earnings — a 41% discount to its peer group median P/E of 24.7x. This discount exists because the market has two legitimate questions: (1) are FY26 margins sustainable or peak-cycle, and (2) does the heavy registration capex suppress FCF for too long?

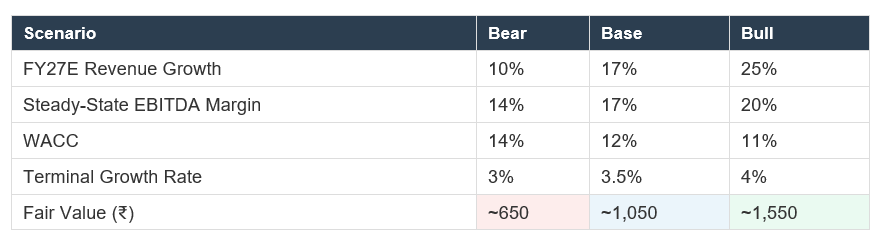

My three-scenario DCF produces the following range:

Probability-weighted fair value (Bear 25% / Base 50% / Bull 25%): ~₹1,075

At CMP of ₹880–906, the stock trades at roughly a 17–20% discount to base-case fair value. This is not a deep-value entry — the margin of safety is moderate, not exceptional. The re-rating case depends on two things: Q4 FY26 results confirming annual PAT above ₹460–500 crore, and management maintaining the FY27 margin guidance of 18–20%.

Risks — Do Not Skip This Section

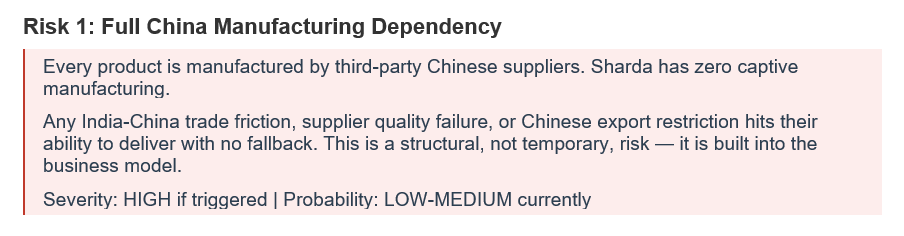

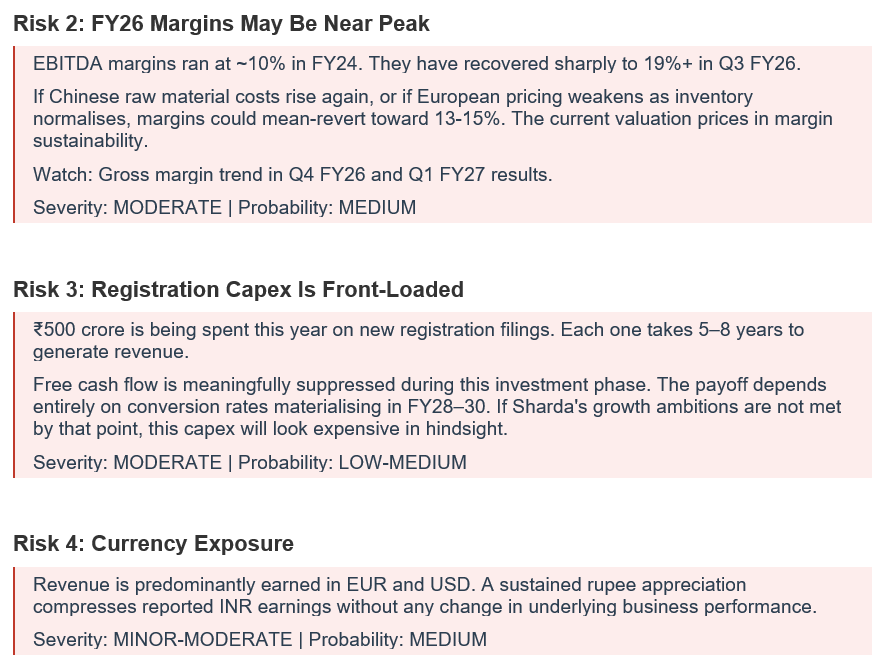

This is the section that matters most. Every number in this note can look right and the investment can still go wrong. These are the six risks I identified:

Verdict

Sharda Cropchem is a genuinely differentiated business. The registration moat is real, the balance sheet is clean, and the earnings recovery is confirmed by hard numbers — not management guidance alone. Rajiv Khanna re-entering after watching the full cycle play out is a signal worth taking seriously.

At CMP ~₹880–906, the stock offers a moderate margin of safety — not a steal, but reasonable compensation for a quality compounder in a recovery phase. The base-case fair value of ~₹1,050 implies a 15–20% return from current levels, with earnings growth compounding on top of that if FY27 guidance materialises.

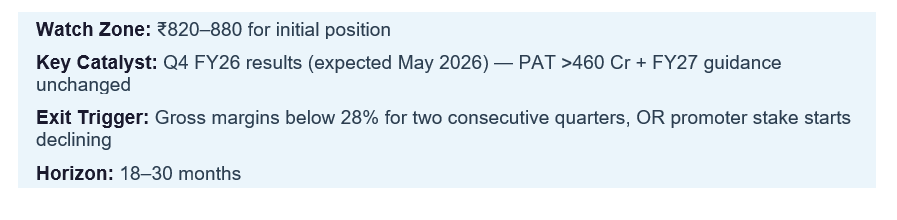

My personal watch zone for an initial position is ₹820–880. I would want to see Q4 FY26 results before sizing up — specifically looking for full-year PAT above ₹460 crore and unchanged FY27 guidance.

Disclaimer

This article is published for educational and informational purposes only. It does not constitute investment advice, a buy or sell recommendation, or a solicitation of any kind. The author is an individual writing in a personal capacity and is NOT a SEBI registered research analyst, investment advisor, or portfolio manager.

All information contained in this article is based on publicly available data including company filings, exchange disclosures, and third-party financial data platforms. While every effort has been made to ensure accuracy, the author makes no representations or warranties of any kind regarding the completeness, accuracy, or reliability of the information. Financial data may have changed since the time of writing.

Investments in securities markets are subject to market risks. The value of investments may go up or down. Past performance is not indicative of future results. The securities mentioned in this article are used solely to illustrate analytical concepts and do not constitute a recommendation to buy, sell, or hold any security.

The author may or may not hold positions in the securities discussed. Any such positions, if held, are disclosed as a conflict of interest for transparency. Readers are strongly advised to conduct their own independent research and consult a SEBI registered financial advisor before making any investment decision.

Please read all scheme-related documents carefully before investing. The author shall not be held responsible for any losses, direct or indirect, arising from the use of information in this article.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.