ESSAY

Shree Refrigerations Limited

31 May 2026

Why I pulled this one apart

Every few weeks a small defence stock starts trending and the same thing happens. The headline screams profit up 300 percent, the comments fill with rocket emojis, and almost nobody opens the filings. So before I put this on a reel, I sat with the numbers properly. Shree Refrigerations builds the cooling and air conditioning systems that go inside Indian Navy warships, and its second half of FY26 was genuinely strong. But a strong six months is not a thesis. This note walks through the business exactly the way I assess anything for my own money, stage by stage, and it is deliberately honest about the parts I do not love.

One thing up front, because it matters. I am not a SEBI registered Research Analyst yet, that registration is in process. So you will not find a buy, sell, target or entry price anywhere in this note. What you will find is the full evaluation, the math, the assumptions, and the risks, so that you can reach your own decision or take it to a registered adviser.

Understanding the business

Shree Refrigerations Limited (SRL) was incorporated in 2006 and operates out of Karad in Maharashtra, with a new facility at Satara inaugurated on 20 May 2026. It designs and manufactures chillers, air and water cooled condensing units, marine HVAC equipment and spray dampening systems. In plain language, it makes industrial grade cooling. The part that gives it an identity is the defence orientation. SRL supplies mission critical refrigeration and HVAC to the Indian Navy for warships and other critical applications, and that is the segment driving the current story.

Revenue is overwhelmingly product led, with the products division contributing around 97 percent and services the small remainder. Three demand pools sit underneath the company. First, defence and naval cooling, which is lumpy, government driven and high value. Second, general industrial HVAC and refrigeration for the domestic market. Third, an emerging line, data centre cooling, where the company has announced a strategic tie up with a global data centre cooling solutions provider.

How I think about the model

This is a project plus product engineering company, not a pure product brand. That means revenue is recognised as orders are executed, costs like manpower are often incurred before the revenue lands, and any single large order can swing a quarter. Keep that rhythm in mind because it explains almost everything in the FY26 numbers.

Industry and macro backdrop

The tailwind here is real and it is not a story I had to invent. India is in the steepest naval expansion of its history. The Navy is set to commission a record 19 warships in 2026, the largest single year addition ever, and after the commissioning of INS Tamal in mid 2025, every new warship is to be built in India. On top of that, the Defence Acquisition Council has cleared a plan for 74 more warships, comprising surface ships and submarines, worth about ₹2.35 lakh crore. Crucially, that figure is an Acceptance of Necessity, a procurement clearance, not awarded contracts, so it signals direction rather than confirmed orders.

Why does this matter for a cooling company? Because HVAC on a warship is not a comfort feature, it is a mission system. The radar, weapons electronics, combat management computers and machinery all generate heat in sealed compartments, and they fail without thermal management. Naval HVAC is governed by stringent military specifications, which means an approved, qualified vendor enjoys a structurally protected position. Every new hull in that pipeline needs this category of equipment.

The second macro leg is data centres. India is in the middle of a data centre build out, and cooling is one of the largest and most R&D intensive cost centres in that industry. SRL’s tie up with a global cooling player is small today, but it points the company at a structurally growing, non lumpy market that could one day balance the defence cyclicality. I treat it as an option, not a base case.

The moat

I do not think SRL has a wide moat, and I would be cautious of anyone who tells you it does. What it has is a narrow but genuine one, built on three things.

1. Defence qualification. Getting approved as a naval HVAC supplier takes years of testing and trust. That approval is the real barrier, and it is why incumbents tend to keep winning repeat orders rather than being displaced on price.

2. Engineering and integration capability. These are custom, made to order systems for demanding environments. The work sits in design, qualification and on site commissioning, which is hard to commoditise.

3. Switching friction. Once a vendor’s equipment is specified into a ship class, the Navy has every reason to stay with it for spares, servicing and follow on vessels of the same class. The recent small spare part orders for B class ships are evidence of this annuity tail.

The honest counterpoint. This is a small company in a field with larger, better capitalised players, including established marine HVAC names globally and domestic engineering majors. The moat protects existing relationships well. It does not guarantee SRL wins the next generation of green refrigerant or natural refrigerant systems, which is a real medium term question I will return to in the risk register.

Management and ownership

SRL is promoter run, led by Chairman and Managing Director Ravalnath Gopinath Shende, with family members including Rajashri Shende and Devashree Nampurkar in the promoter group. The company listed on the BSE SME platform on 31 July 2025 at an issue price of ₹125, and opened around ₹169.85, a listing gain of roughly 36 percent. The IPO raised ₹117.33 cr, of which ₹94.51 cr was a fresh issue and ₹22.81 cr an offer for sale. Post issue, promoter holding came down from about 56.6 percent to about 44.59 percent, which is the normal dilution of an IPO rather than a signal in itself.

The capital allocation move I want to flag positively is the deliberate H1 FY26 investment ahead of the order ramp. Management expanded headcount from 247 to 323 and added shop floor capacity, knowing it would dent near term margins. That is the correct sequencing if you genuinely believe the orders are coming, and H2 results suggest the bet paid off. The flip side is that I would like several more quarters of evidence that this was strategy and not just timing luck, given how short the listed track record is.

Smart money, stated accurately

Ashish Kacholia held 3.42 percent as of the March 2026 shareholding pattern. This is a holding, not a fresh open market purchase, and a defence focused fund (Maharashtra Defence and Aerospace Venture Fund) actually trimmed a small stake recently. I mention all three together so the picture is balanced. The presence of a respected investor is a soft positive, not a reason to buy, and I would always verify the latest filed shareholding before relying on it.

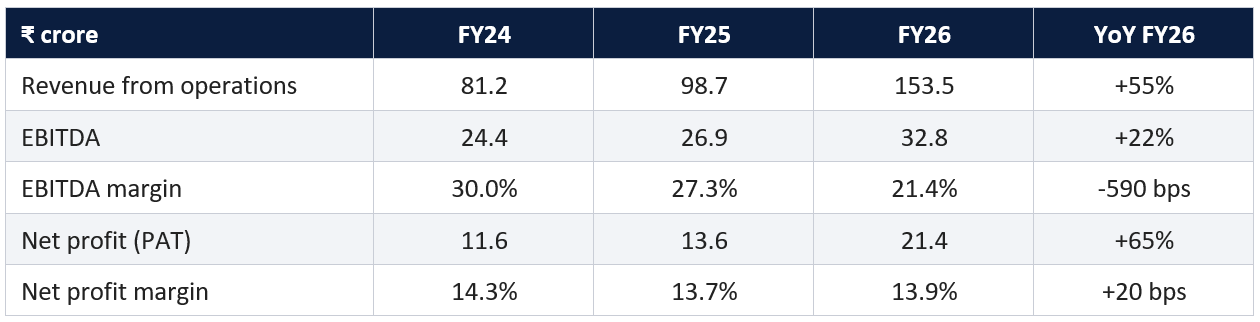

The financials

Here is the three year picture, then the half year split that explains the FY26 headline.

Figures rounded. FY24 and FY25 from restated and reported results, FY26 from the audited results approved on 10 May 2026.

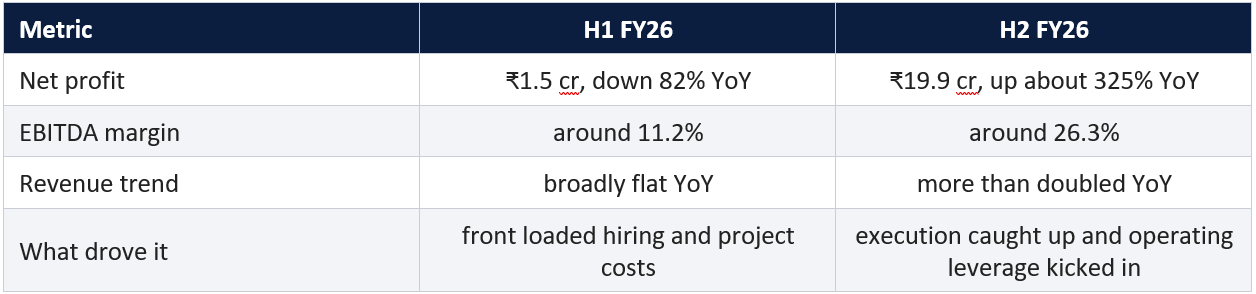

The story is in the two halves

If you only read the full year, you miss what happened. FY26 was a tale of two very different halves.

This is the single most important thing to understand about the stock. The dramatic full year growth is real, but it is heavily back ended into one strong half that followed one weak half. The bull reads this as operating leverage finally showing up. The bear reads it as a low base in H1 flattering the H2 comparison. Both are partly right, and the honest position is that we need to see whether H2 FY26 was the new run rate or a bunching of deliveries. I am not willing to annualise a single strong half and call it the trend.

Balance sheet and returns

This is where SRL looks genuinely solid. Debt to equity is just 0.17, so this is not a leveraged story. Cash and equivalents jumped to ₹57.5 cr from ₹5.9 cr a year earlier, almost entirely the IPO proceeds, and net worth rose to ₹219.6 cr. Total assets grew to ₹299.9 cr from ₹188.7 cr. Returns are decent but not spectacular: ROCE of 13.9 percent and ROE of 13.0 percent for FY26. For a re rating to be justified, those returns need to climb as the new capacity gets utilised, and that is an output to track, not an assumption to bank.

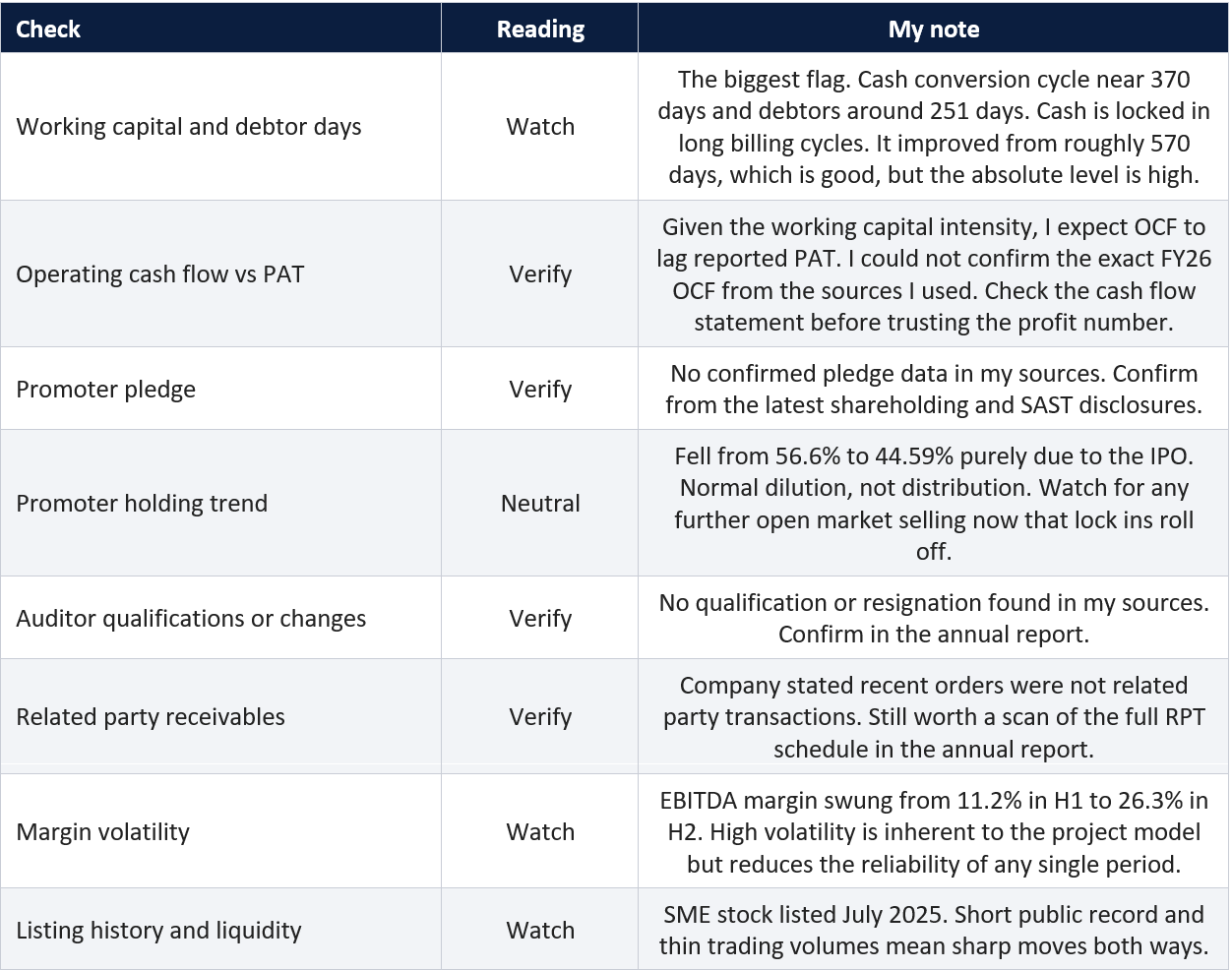

Stage 6. Forensic red flag checklist

I run this on every company, even the clean looking ones. Here is the honest scorecard.

Stage 7. Valuation and scenario analysis

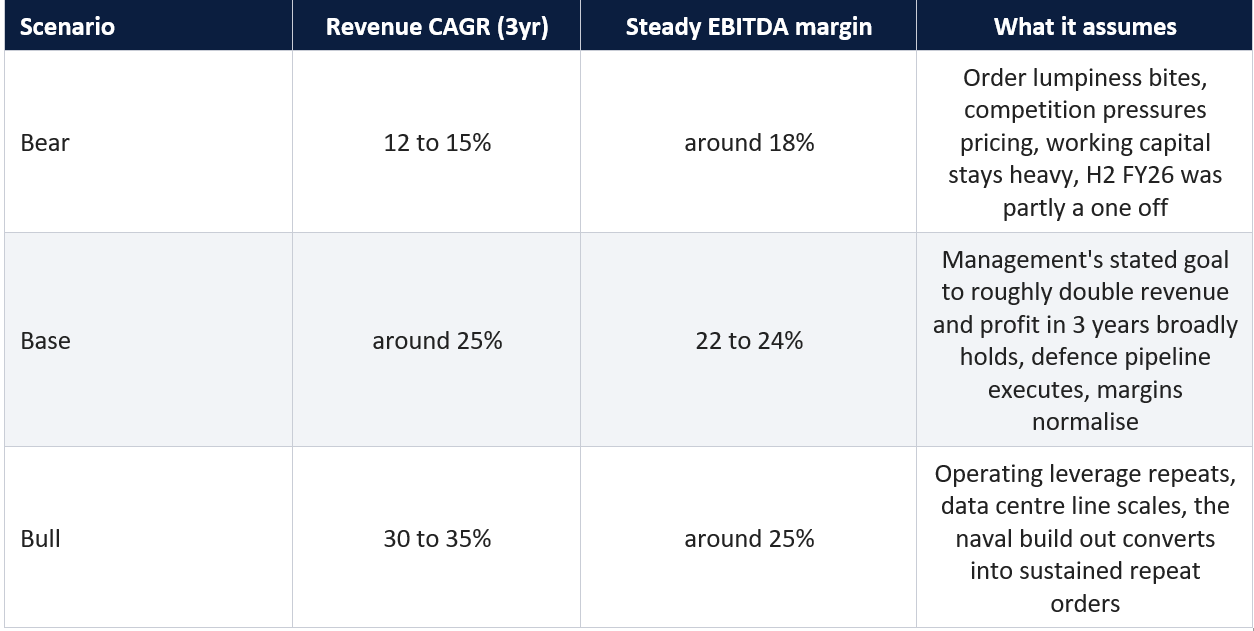

This section is illustrative scenario analysis, not a price target and not a recommendation. Its only purpose is to show how the value of this business changes under different assumption sets, so you can judge what the market is currently pricing in.

First, where the market sits. Depending on the date, SRL has traded around ₹737 cr to ₹900 cr in market capitalisation, on a trailing price to earnings ratio in the high 40s to mid 50s and a price to book of roughly 3.5 to 6.4. The 52 week range is wide, ₹153 to ₹311.5. So the market is already paying a growth multiple. The question scenario analysis helps answer is what growth that multiple demands.

A note on method. Because SRL has a heavy working capital cycle, a classic discounted cash flow based on profit would overstate the cash it actually generates. Free cash flow is materially below reported profit until that cycle tightens. So I anchor the scenarios on a forward earnings power and a sensible exit multiple, and I treat the output as a range of implied business values, not a target.

Reading the scenarios honestly: the base case requires the company to deliver close to a doubling of earnings over three years and to hold the better H2 margins. If it does, today’s multiple is demanding but not absurd for a defence linked grower. The bear case, where growth slows and margins sit nearer 18 percent, would leave the current valuation looking expensive and vulnerable to a de rating. The bull case is genuinely attractive but rests on two things repeating that have so far been demonstrated for only one half year. I want to stress the asymmetry: a lot of good news is already in the price, so the burden of proof sits with execution.

The one line valuation summary

At the current multiple, the market is already paying for the base case to happen. The interesting work for an investor is not modelling the bull case, it is stress testing whether the bear case is adequately priced. That is a personal risk judgement, not something I can or will make for you.

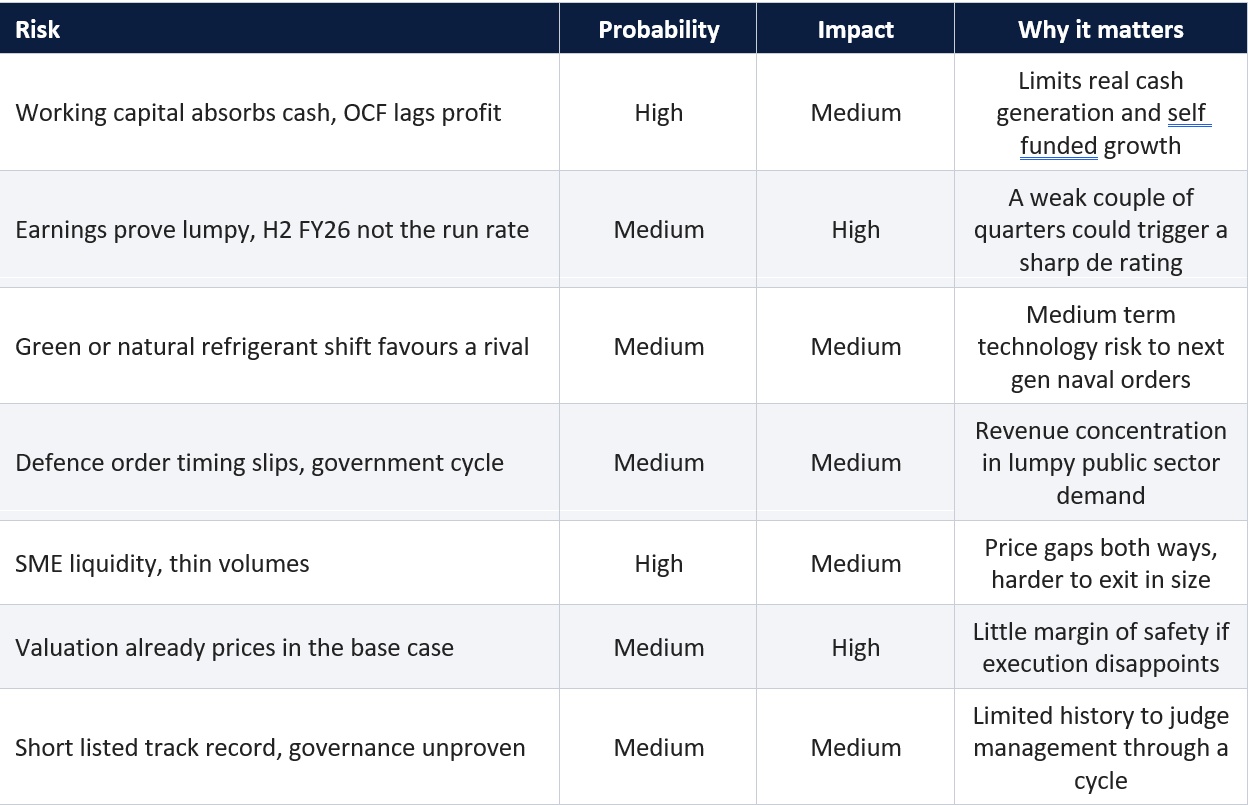

Stage 7b. Risk register

Probability and impact are my qualitative judgement, scored Low, Medium or High.

My five sentence summary

1. Shree Refrigerations is a small, founder run, defence oriented HVAC manufacturer that supplies mission critical cooling to the Indian Navy, sitting in front of a record naval shipbuilding cycle.

2. FY26 looked excellent on the surface, revenue up 55 percent and profit up 65 percent, but almost all of that strength is concentrated in a single strong second half that followed a deliberately cost heavy first half.

3. The balance sheet is a genuine strength, very low debt and a large post IPO cash pile, while returns at around 13 percent are respectable but not yet exceptional.

4. The clearest things to watch are the high working capital cycle and the question of whether the strong H2 margins are repeatable, and the valuation already appears to price in the base case of continued strong growth.

5. This is a watch and verify situation in my own framework, where the next two or three quarters of cash flow and margin data will tell you far more than any single headline, and none of this is a recommendation to act.

What I will be tracking from here

• Operating cash flow versus reported profit in the FY26 annual report, and whether the working capital cycle keeps tightening below 370 days.

• Whether H2 FY26 margins of around 26 percent hold up in H1 FY27, or whether they fade back toward the low twenties.

• Fresh order inflows, especially any new naval awards beyond the existing Fleet Support Ship work, and progress on the data centre cooling tie up.

• The next filed shareholding pattern, for any change in promoter holding or in the institutional names on the register.

• Any move toward green or natural refrigerant systems, which would tell me whether SRL is positioned for the next generation of naval cooling or at risk of being leapfrogged.

Important disclaimer and disclosures

This note is published for educational and informational purposes only. It is my personal analysis and opinion as an individual writing under the Compound with Raunak banner.

I am not registered with the Securities and Exchange Board of India (SEBI) as a Research Analyst or as an Investment Adviser. Nothing in this document is investment advice, a research report as defined under the SEBI (Research Analysts) Regulations, or a recommendation, solicitation or offer to buy, sell or hold any security.

This note deliberately contains no buy, sell or hold call, no target price and no entry or exit price. The scenario analysis is illustrative and is intended only to show how value responds to different assumptions. It must not be read as a forecast or a price target.

All figures are sourced from publicly available exchange filings, company disclosures and reputable financial media, and were believed accurate as of 31 May 2026. Data may contain errors, may have been revised, or may have changed after publication. Always verify every number against the company’s primary filings before relying on it.

Securities markets carry risk and you can lose money, including your entire capital. Small and medium enterprise (SME) platform stocks are especially high risk, can be illiquid, and can move sharply. Past performance is not indicative of future results.

I may hold positions in this stock.

You are solely responsible for your own investment decisions. Please do your own research and consult a SEBI registered investment adviser who can take your personal financial situation into account before making any decision.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.