ESSAY

The ₹104 Crore Dilution Trap: Decoding Madhusudan Kela’s 7% Stake in Subam Papers

13 March 2026

When billionaires start injecting hard cash into companies with a market cap of barely ₹390 Crores, it warrants a deep dive into the exchange filings. Let’s strip away the hype and look at the raw mathematical reality of this preferential allotment, the growth catalysts, and the terrifying red flags hiding in their balance sheet.

The ₹104 Crore Capital Infusion

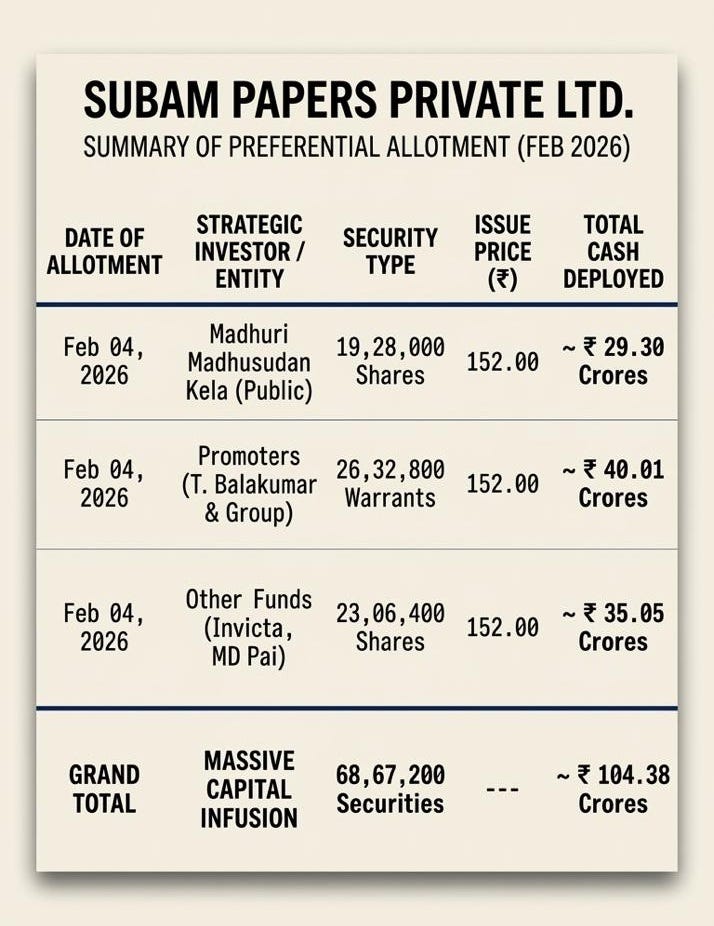

On February 4, 2026, the Board of Directors of Subam Papers approved a massive Preferential Allotment to raise exactly ₹104.38 Crores.

For the uninitiated, a “Preferential Allotment” is when a company issues brand-new shares directly to strategic investors, bypassing the open market. Here is exactly who bought in and at what price:

Note on Warrants: While the public investors paid 100% upfront for equity shares, the promoters issued themselves convertible warrants. By law, they only need to pay 25% of the ₹40 Crores upfront, with the remaining 75% due within 18 months upon conversion to equity.

The Bull Case: Why is Smart Money Buying?

You don’t deploy ₹30 Crores into a micro-cap without a clear line of sight on future earnings. The thesis here is straightforward: Aggressive Expansion & Debt Restructuring.

Subam Papers is historically a manufacturer of kraft paper and paper products. However, the packaging industry is highly capital-intensive. The ₹104 Crore war chest serves two immediate purposes:

Wiping Out Debt: A significant portion of these proceeds will be aggressively deployed to prepay existing high-interest bank borrowings. Wiping out legacy debt instantly cleans up the balance sheet and dramatically improves bottom-line profitability.

The Corrugated Box Unit: The company is executing a massive forward-integration strategy. They are pumping funds into their wholly-owned subsidiary, “Subam Paper & Boards Private Limited,” to set up a brand-new corrugated box manufacturing unit. This allows them to capture higher margins in the final packaging stage rather than just selling raw paper.

When promoters commit ₹40 Crores of their own capital alongside marquee investors to fund an expansion, it is the ultimate “skin in the game” signal.

The Bear Case: The 3 Massive Red Flags

Before you rush to buy the stock just because a billionaire did, you must look at the dark side of this transaction.

1. The Equity Dilution Trap (The EPS Crush)

This is the biggest risk that retail investors fundamentally misunderstand. A preferential issue is not free money. To raise this ₹104 Crores, Subam Papers literally had to expand its authorized share capital and create over 68.6 Lakh brand new securities out of thin air.

When a company prints millions of new shares, it “dilutes” the ownership percentage of existing shareholders. More importantly, in the short term, their Earnings Per Share (EPS) will artificially collapse. The company will be dividing the exact same net profit among a significantly larger pool of shares. Unless the new corrugated unit starts generating massive profits immediately to offset the new shares, the valuation will look incredibly expensive.

2. Extreme Micro-Cap Illiquidity

With a market capitalization hovering around ₹390 Crores, Subam Papers is a pure micro-cap. These stocks are notoriously illiquid. While a ₹104 Crore cash injection is a phenomenal growth catalyst, micro-caps are highly vulnerable to broader market sentiment. If the market corrects, or if operators decide to dump, stocks of this size can get locked in lower circuits, trapping retail liquidity entirely.

3. Raw Material Cyclicality & Margin Compression

The paper and packaging industry is a brutal, low-margin business heavily dependent on the highly volatile prices of waste paper, kraft paper, and freight costs. Subam Papers has historically suffered from tight EBITDA margins. If input costs spike before they finish building their new expansion unit, their operating margins will be severely compressed, wiping out the benefit of their debt reduction.

The Verdict

Subam Papers is a classic, high-risk turnaround play. The massive ₹104 Crore cash infusion, backed by the Kela family and the promoters, gives them the ultimate war chest to dominate their packaging niche.

However, positional investors must be incredibly careful regarding the incoming EPS dilution. The smart move is to track their upcoming quarterly results to see how fast they can deploy this capital and whether the new corrugated box unit actually impacts the bottom line.

Watch the execution, not just the headlines.

⚠️ DISCLAIMER: I am not a SEBI-registered investment advisor. This article is strictly for educational and informational purposes only and does not constitute financial advice. The data presented is based on public exchange filings and market research. I may or may not hold positions in the discussed stock. Micro-cap investments carry extreme risk, including the total loss of capital. Always consult a certified financial advisor and perform your own rigorous due diligence before making any investment decisions.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.