ESSAY

The ₹62 Crore Insider Bet: My Complete DCF Valuation of NCC Limited

16 March 2026

As a fundamental investor, I don’t just follow the smart money blindly. When promoters start deploying tens of crores of their own personal cash into their own stock, it is a massive signal, but it still requires rigorous mathematical validation.

Today, we are stripping away the market noise, the election fears, and the media headlines. We are going to look strictly at the intrinsic cash-flow generation capability of NCC.

Here is my complete Discounted Cash Flow (DCF) valuation model, explaining exactly why the Alluri family just bought the dip, and what this infrastructure giant is actually worth.

The Investment Thesis: The Working Capital Bottom

Before we look at the spreadsheet, you have to understand the narrative dislocation.

Recently, NCC’s stock corrected by nearly 30-40%. The retail market panicked because the company’s gross debt spiked to nearly ₹2,980 Crores in Q3. What the retail crowd missed was why that debt spiked. State governments severely delayed paying NCC for completed Jal Jeevan Mission (water infrastructure) projects, temporarily choking their working capital.

The promoters deployed ₹62 Crores to buy the dip because they know this is a temporary timing mismatch. Management just confirmed they recovered over ₹560 Crores of that trapped cash in January alone, and simultaneously bagged another ₹2,400+ Crores in fresh orders.

With a record-breaking order book of ₹79,571 Crores, the working capital cycle has officially bottomed out. Now, let’s build the model.

Part 1: Cost of Capital (WACC) Assumptions

To value a highly cyclical infrastructure company, we need a conservative discount rate that accurately reflects the macroeconomic environment and the inherent execution risks.

Risk-Free Rate: 6.70% (Yield on the India 10-Year Government Bond)

Equity Risk Premium: 6.00% (Standard premium for the Indian equity market)

Beta (β): 1.20 (Adjusted for the higher volatility of the infra sector)

Cost of Equity (Ke): 13.90% (CAPM model)

Cost of Debt (Kd - Post Tax): 7.80% (Assuming ~10.4% borrowing cost and a 25% corporate tax rate)

Target Capital Structure: 75% Equity / 25% Debt

Weighted Average Cost of Capital (WACC): 12.50%

We will discount all future cash flows back to today using this 12.50% hurdle rate.

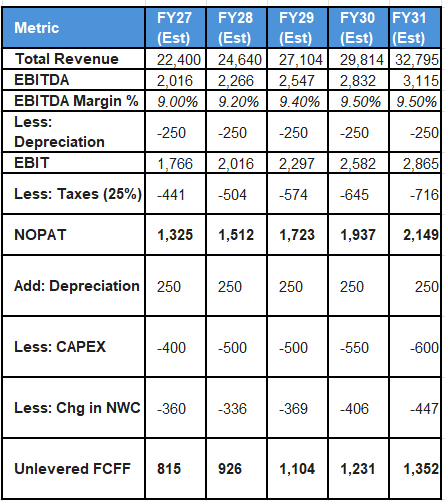

Part 2: Free Cash Flow Projections (FY27 - FY31)

All figures in ₹ Crores.

The Growth Rationale: Valuing NCC purely on its ₹79,571 Cr order book, I am projecting a highly conservative 10-12% annual revenue growth. As execution ramps up on higher-margin Metro and Smart City projects, I expect EBITDA margins to structurally expand from the current ~8.9% to 9.5% by FY30.

(Note: FY27 CAPEX is modeled exactly on management’s ₹400 Cr guidance. Changes in Net Working Capital are modeled at a strict 15% of incremental revenue to account for standard government receivable delays).

Part 3: Enterprise Value & Intrinsic Target

To calculate the Terminal Value (what the company is worth after FY31), I assumed a perpetual growth rate of 4.0%. This perfectly mirrors India’s long-term real GDP growth floor, infrastructure companies cannot outgrow the broader economy in perpetuity.

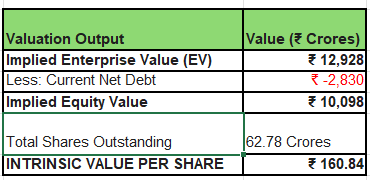

Terminal Value Calculation: ₹1,352 Cr * (1.04) / (12.5% - 4.0%) = ₹16,541 Crores

Present Value of 5-Yr Cash Flows: ₹3,748 Crores

Present Value of Terminal Value: ₹9,180 Crores

The Final Verdict: The Margin of Safety

At the current market price of around ₹144, NCC is trading at a roughly 11% to 12% discount to its intrinsic cash flow value of ₹161.

This mathematical margin of safety is exactly why the promoters stepped in. If you look at the exchange filings, the insider group acquired their latest block of shares at an average price hovering between ₹133 and ₹140. They bought right at the absolute floor of this valuation model.

NCC is severely mispriced by a retail market that only reads the headlines and panics at temporary debt spikes. For investors willing to absorb short-term political and election volatility, this stock offers a highly asymmetric risk-to-reward ratio backed by a colossal, execution-ready order book.

Watch the execution, not the noise.

⚠️ DISCLAIMER: I am an individual research analyst. This article and the financial models provided are strictly for educational and informational purposes only, and do not constitute financial advice. The data presented is based on public exchange filings, management commentary, and my personal market research. I may or may not hold positions in the discussed stock. Equities carry extreme risk, including the total loss of capital. Always consult a certified financial advisor and perform your own rigorous due diligence before making any investment decisions.

WANT MORE LIKE THIS?

Join the Inner Circle for weekly deep-dives and live trade calls.

Apply for accessCompound with Raunak is not a SEBI-registered investment adviser. All content published on this platform, including trade calls, research, and analysis, is for educational and informational purposes only. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Readers should consult a qualified financial adviser before making investment decisions. Past performance is not indicative of future results.